Search

More results...

Exact matches only

Search in title

Search in content

Filter by Custom Post Type

Search results after date:

dd-mm-yy

What I Really Want to Say

Blog

What I Really Want to Say

Still Worth Reading

Lost Causes and Other Necessary Deeds

Archives

CNBC Archives

Inc. Archives

SF Gate Archives

Archives

Metro Archives

Harvard Business School

Hal’s Scrapbook

About Hal Plotkin

Bio

Contact

CV / Publication List

What I Really Want to Say

Blog

What I Really Want to Say

Still Worth Reading

Lost Causes and Other Necessary Deeds

Archives

CNBC Archives

Inc. Archives

SF Gate Archives

Archives

Metro Archives

Harvard Business School

Hal’s Scrapbook

About Hal Plotkin

Bio

Contact

CV / Publication List

November 2008

Featured

What I Really Want to Say

#MeToo — It Doesn’t Only Happen to Women

22nd October 2017

Featured

What I Really Want to Say

Two Big Reasons for Hope: The Platform Cooperative Consortium Lights Up The Commons.

24th January 2017

Featured

What I Really Want to Say

Five Bold New Progressive Ideas for California’s Next U.S. Senate Race

2nd December 2016

Featured

What I Really Want to Say

The Fast-Growing Academic Conference — That Shouldn’t Be Happening in the First Place.

5th October 2016

Still Worth Reading

What I Really Want to Say

Hillary Clinton’s Big Jobs Mistake

29th July 2016

Still Worth Reading

What I Really Want to Say

Governor Jerry Brown’s Huge Gift to California Community College Students: Free Textbooks

30th June 2016

What I Really Want to Say

Introducing SLAVER — New iPhone App

21st April 2016

Featured

What I Really Want to Say

A Funnie [sic] Letter from Textbook Publishers to California’s Governor

29th March 2016

Featured

What I Really Want to Say

Who Owns Digital Learning Resources Funded by Taxpayers?

3rd March 2016

Still Worth Reading

What I Really Want to Say

What a Real “Skills Gap” Looks Like

11th February 2016

What I Really Want to Say

Making Open Education History In Mexico at the 2015 OGP Meeting

24th October 2015

Featured

Lost causes and other necessary deeds

Still Worth Reading

Here’s How Open Academic Tests Would Work

23rd May 2015

Featured

What I Really Want to Say

An Open Educational Resources Agenda for President Obama

17th April 2015

Featured

Lost causes and other necessary deeds

What I Really Want to Say

Cold Comfort: $10 Billion Dollars Later LA Times Says I Got it Right

5th April 2015

What I Really Want to Say

The Zombie Skills Gap Argument Again?!

17th March 2015

What I Really Want to Say

Victory Unclaimed: Obama’s Investments in Open Educational Resources

17th March 2015

What I Really Want to Say

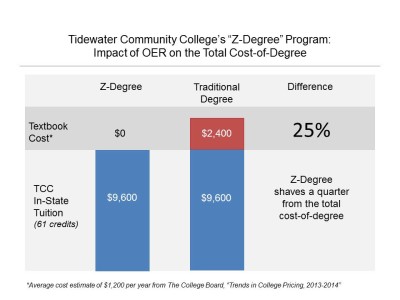

Tidewater’s Z-Degree Concept Gets Traction

24th February 2015

What I Really Want to Say

Winning “Why Open Education Matters” Video

23rd February 2015

Featured

What I Really Want to Say

Rootstrikers: Building a New Operating System for Leaders

20th February 2015

Featured

What I Really Want to Say

You Talkin to Me?

20th February 2015

Featured

What I Really Want to Say

Thank you, Martha Kanter

20th February 2015

Featured

What I Really Want to Say

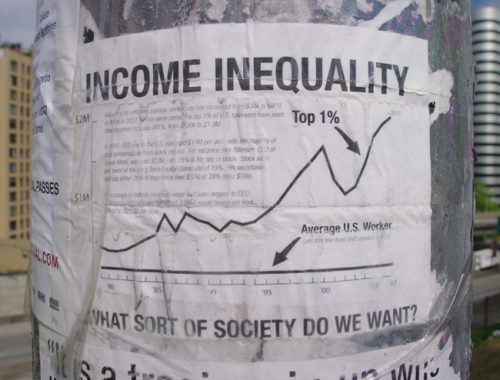

Weintraub Cites Kenworthy’s Work on Income-Inequality

2nd February 2015

What I Really Want to Say

California Health Care Coalition

22nd January 2015

What I Really Want to Say

Obama Initiative Boosts Community Colleges and OER

22nd December 2014

What I Really Want to Say

Edward Kennedy’s Eulogy for His Brother Bobby

22nd December 2014

What I Really Want to Say

President Obama Proposes Online Skills Laboratory

22nd December 2014

What I Really Want to Say

Education Secretary Arne Duncan’s 21st Century Vision

22nd December 2014

What I Really Want to Say

D.C. Lobbyists Protest Obama Change in Policy

22nd December 2014

What I Really Want to Say

John Fensterwald’s New Education Blog

22nd December 2014

What I Really Want to Say

Foothill College Houses Center for Open Educational Resources

22nd December 2014

What I Really Want to Say

Education Secretary Arne Duncan: Banks vs. Students

22nd December 2014

What I Really Want to Say

White House Releases Documents on Proposed Higher Ed Reforms

22nd December 2014

What I Really Want to Say

Big Ideas Fest Talk on Obama Administration Higher Education Priorities

22nd December 2014

What I Really Want to Say

Harris Mankin (aka Harry Boswell), RIP

22nd December 2014

Still Worth Reading

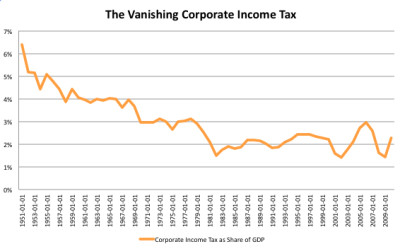

The Truth About U.S. vs. Foreign Corporate Tax Rates

22nd December 2014

What I Really Want to Say

Jon Stewart Takes On the Fox News Smear Machine

22nd December 2014

What I Really Want to Say

Creative Commons Publishes my “Free to Learn” OER Guide

22nd December 2014

Still Worth Reading

My First Ever Post on the White House Blog

22nd December 2014

What I Really Want to Say

Who Will Protect California’s Students?

22nd December 2014

What I Really Want to Say

Open Educational Resources and the Obama Administration

22nd December 2014

What I Really Want to Say

Why Open Education Matters” Video Contest Launches

22nd December 2014

Open Letter to Foothill De Anza Faculty

17th November 2014

What I Really Want to Say

Why Open Education Matters Video Contest Launches

1st March 2012

Still Worth Reading

Who Will Protect California’s Students?

1st July 2011

What I Really Want to Say

Open Educational Resources and the Obama Administration

1st May 2011

What I Really Want to Say

Public Invited to My Talk At Google HQ in Mountain View

29th March 2011

What I Really Want to Say

My First Ever Post on the White House Blog

1st January 2011

What I Really Want to Say

Creative Commons Publishes my “Free to Learn” OER Guide

1st October 2010

What I Really Want to Say

The Truth About U.S. vs. Foreign Corporate Tax Rates

1st August 2010

What I Really Want to Say

Jon Stewart Takes On the Fox News Smear Machine

1st August 2010

What I Really Want to Say

Harris Mankin (aka Harry Boswell), RIP

1st March 2010

What I Really Want to Say

Education Secretary Arne Duncan: Banks vs. Students

1st February 2010

What I Really Want to Say

John Fensterwald’s New Education Blog

1st November 2009

What I Really Want to Say

Education Secretary Arne Duncan’s 21st Century Vision

1st October 2009

What I Really Want to Say

Short History of OER and Community Colleges

1st October 2009

What I Really Want to Say

D.C. Lobbyists Protest Obama Change in Policy

1st October 2009

What I Really Want to Say

President Obama Proposes Online Skills Laboratory

1st September 2009

What I Really Want to Say

Edward Kennedy’s Eulogy for His Brother Bobby

1st August 2009

What I Really Want to Say

Obama Initiative Boosts Community Colleges and OER

1st July 2009

What I Really Want to Say

Foothill-De Anza Makes Dreams Come True. Trust me. I know.

1st June 2009

What I Really Want to Say

Bruce Springsteen’s “Land of Hope and Dreams”

1st May 2009

What I Really Want to Say

Carl Guardino vs. President Obama

1st May 2009

What I Really Want to Say

ReelChanges “Heist” Project Raised $30K Today!

1st May 2009

What I Really Want to Say

ReelChanges.org Documentary Project Raises $5K in One Day!

24th April 2009

What I Really Want to Say

Undersecretary of Education Dr. Martha Kanter!

1st April 2009

What I Really Want to Say

PBS Trade Journal CURRENT Features Story on ReelChanges.org

1st April 2009

What I Really Want to Say

CBS Pulls Last Week’s (4/19) “60 Minutes” Broadcast Off Web!?

1st April 2009

What I Really Want to Say

Banking on Trouble Ahead

28th March 2009

What I Really Want to Say

SFGate.com Features Story on Spot.us

17th March 2009

What I Really Want to Say

Free Textbooks at Foothill-De Anza: First Annual Report

6th March 2009

What I Really Want to Say

We Must Stop Conyers Misguided H.R. 801

2nd March 2009

What I Really Want to Say

Why Richard Alexander is the Best Personal Injury Attorney

27th February 2009

What I Really Want to Say

Bring Back Usury Laws To Hasten Economic Recovery

26th February 2009

Still Worth Reading

Bring Back Usury Laws To Hasten Economic Recovery

26th February 2009

What I Really Want to Say

Spot.us and ReelChanges Make The Guardian Website Today

24th February 2009

What I Really Want to Say

Maryland Public Television and ReelChanges.org Debut New Fundraising Approach

14th February 2009

What I Really Want to Say

ReelChanges.org Site Working Again

31st December 2008

What I Really Want to Say

DOS Attack Takes Down ReelChanges.org

26th December 2008

What I Really Want to Say

A Few Bad Apples or A Bad Orchard?

19th December 2008

Lost causes and other necessary deeds

Corporation for Public Broadcasting Gives Innovation Grant to ReelChanges!

5th December 2008

Lost causes and other necessary deeds

Feds Bailout Obsolete Banking Business Model

25th November 2008

What I Really Want to Say

USA 2008: RIP?

24th November 2008

Lost causes and other necessary deeds

Money for Citibank?

22nd November 2008

Lost causes and other necessary deeds

Still Worth Reading

How to End the Credit Crunch

16th November 2008

What I Really Want to Say

David Cohn Tells It Like It Is

14th November 2008

What I Really Want to Say

First ReelChanges Doc Project Tops $2K in Contributions!

26th October 2008

What I Really Want to Say

ReelChanges Wins Nice Grant from Google!

13th October 2008

What I Really Want to Say

B’Nai Darfur (“Sons of Darfur”): Best ReelChanges Documentary Project Yet?

9th September 2008

What I Really Want to Say

Los Angeles Times Covers our Free Textbook Project

24th August 2008

What I Really Want to Say

Today’s New York Times Features Spot.Us!

18th August 2008

What I Really Want to Say

ReelChanges Homepage Already Fully Populated!

5th August 2008

What I Really Want to Say

My New Project Launches: ReelChanges.org

1st May 2008

What I Really Want to Say

Jokerman by Bob Dylan

14th April 2008

What I Really Want to Say

Google’s “White Space” FCC Proposal Heralds New Day for Telecom and Broadcasting

24th March 2008

What I Really Want to Say

Eeeek! I lost everyone’s email address!

22nd March 2008

What I Really Want to Say

Hewlett Packard is Back: Stock Price to Follow?

21st March 2008

What I Really Want to Say

Memo to Blogosphere: Let’s Drop the Term Mainstream Media — “MSM” — and Instead Use Corporate-Owned News Media — “CONM”

18th March 2008

What I Really Want to Say

Must Obama Answer for Rezko, Power and Rev. Jeremiah Wright?

15th March 2008

What I Really Want to Say

Gaining Traction in the Blogosphere

13th March 2008

What I Really Want to Say

Friends Create Obama Works Website

4th March 2008

What I Really Want to Say

Hillary Clinton Plays the Fear Card in Texas

1st March 2008

What I Really Want to Say

Weintraub Cites Kenworthy’s Work on Income-InequalityWeintraub Cites Kenworthy’s Work on Income-Inequality

1st March 2008

What I Really Want to Say

Stanford Finally Waives Tuition for Middle Income Families: It’s About Time

20th February 2008

What I Really Want to Say

My Favorite Tom Lantos Story

14th February 2008

What I Really Want to Say

Obama’s Best Line of the Night: “We Are The Ones We’ve Been Waiting For.”

6th February 2008

What I Really Want to Say

Obama Must Rise Above Clinton’s Fear-Mongering

3rd February 2008

What I Really Want to Say

NAFTA Stance Hurts Obama and Clinton in Silicon Valley; Boosts McCain

1st February 2008

What I Really Want to Say

My Question for Hillary Clinton

25th January 2008

What I Really Want to Say

Obama’s Hope

11th January 2008

What I Really Want to Say

Yes on 92

1st January 2008

What I Really Want to Say

Yes We Can — Obama for President in 2008

1st January 2008

Lost causes and other necessary deeds

Junk Media

13th December 2007

What I Really Want to Say

ABC.com Just Censored Me!

2nd December 2007

What I Really Want to Say

Report Card: Corporate-Owned Media Fails Public Again

28th November 2007

What I Really Want to Say

Lantos vs. Yahoo: John Dvorak Gets It Entirely Wrong

9th November 2007

What I Really Want to Say

Voice Mail Failure Today

31st October 2007

What I Really Want to Say

Leaving AIT for Hostgator

24th October 2007

What I Really Want to Say

Dump Comcast Now

20th October 2007

What I Really Want to Say

Loren with Former Vice President Al Gore

12th October 2007

What I Really Want to Say

Yale University to Offer ADA-Compliant Open Education Resources

28th September 2007

What I Really Want to Say

Updates, Get Your Fresh Updates…

26th September 2007

What I Really Want to Say

Three Questions for the OpenCourseWare Community

1st September 2007

What I Really Want to Say

News Flash: Ruskin’s AB 577 Supports Open Education Resources

2nd March 2007

What I Really Want to Say

The New York Times Covers “Table-Top Fusion”

27th February 2007

What I Really Want to Say

League for Innovation OER Links

22nd February 2007

What I Really Want to Say

Terry McAuliffe for President

14th February 2007

What I Really Want to Say

Bad Experience at Wardman Park Marriott Hotel

12th February 2007

What I Really Want to Say

OER and ACCT in Washington, D.C.

10th February 2007

What I Really Want to Say

Purdue Exonerates Dr. Taleyarkhan — (Update: Then Reverses Decision 8/08)

8th February 2007

What I Really Want to Say

The Strange Case of Dr. Rusi Taleyarkhan

6th February 2007

What I Really Want to Say

Why I Like Joe Biden

31st January 2007

What I Really Want to Say

Proposal: A Three Step Democratic Party Plan for Victory in Iraq

29th January 2007

What I Really Want to Say

Kiva.org Signals Net Evolution

27th January 2007

What I Really Want to Say

Santa Clara County Health Benefits Coalition Organizing Meeting Set

27th December 2006

What I Really Want to Say

OpEd in San Jose Mercury News

20th December 2006

What I Really Want to Say

Is Yahoo! the Next AOL?

14th December 2006

What I Really Want to Say

Race Card Used in Fight Against Network Neutrality

27th November 2006

What I Really Want to Say

Open Educational Resources Talks in Orlando and Charlotte

26th October 2006

What I Really Want to Say

Annual Conference on Open Educational Resources Concludes

30th September 2006

What I Really Want to Say

U.C Berkeley Finally Begins to Broadcast Lectures

28th September 2006

What I Really Want to Say

Health Benefits Coalition Gathers Momentum

21st September 2006

What I Really Want to Say

Pretexting vs. Legitimate Investigative Journalism Techniques

15th September 2006

What I Really Want to Say

Independent Outside Review Panel Needed at H-P

13th September 2006

What I Really Want to Say

Tom Perkins is the Real Face of Silicon Valley

12th September 2006

What I Really Want to Say

The Questions HP Still Must Answer

9th September 2006

What I Really Want to Say

Memo to the Press: Pretexting is Already Illegal

8th September 2006

What I Really Want to Say

Local Health Care Consumers Getting Organized

14th August 2006

What I Really Want to Say

Smart Commentary on the Crisis in the Middle East

22nd July 2006

What I Really Want to Say

Telcos/Cable Firms Seek Net Takeover, as Predicted

7th July 2006

What I Really Want to Say

Vote Yes on Measure C

12th April 2006

What I Really Want to Say

Sacramento Hearing on Public Domain Textbooks

6th March 2006

What I Really Want to Say

Steve Westly for Governor

1st February 2006

What I Really Want to Say

County Health Benefits Coalition Organizing Update

6th January 2006

What I Really Want to Say

Assessing the Financial Value of our Community Colleges

14th November 2005

What I Really Want to Say

An Urgent Situation in Haiti — Please Spread the Word

13th October 2005

What I Really Want to Say

Back to Blogging

13th October 2005

What I Really Want to Say

Cisco Systems Becomes Part of the Stock Option Accounting Solution

13th May 2005

What I Really Want to Say

Health Benefits Forum a Success

14th February 2005

Lost causes and other necessary deeds

Santa Clara County Health Benefits Coalition Organizing Meeting Set

4th February 2005

What I Really Want to Say

Join Us to Keep Health Benefits Affordable

3rd February 2005

What I Really Want to Say

Let’s Reject Unverifiable National Election Results

27th December 2004

What I Really Want to Say

Library to Put 30 Million Public Domain Newspaper Pages Online

2nd November 2004

What I Really Want to Say

An Electronic Coup?

1st November 2004

What I Really Want to Say

Thomas Jefferson on the 2004 Election

1st November 2004

What I Really Want to Say

Evidence of an Electronic Coup?

1st November 2004

What I Really Want to Say

Scientific Panel Will Investigate 2004 Election Methods

1st November 2004

What I Really Want to Say

Bush Won Dirty

1st November 2004

What I Really Want to Say

Electronic Frontier Foundation Seeks Independent Tests of Certain 2004 Voting Machines

1st November 2004

What I Really Want to Say

Losing Our Democracy in Super Slo-Mo

23rd October 2004

What I Really Want to Say

Two More Reporters Have Their Constitutional Rights Violated

19th October 2004

What I Really Want to Say

Creating Public Domain Textbooks

10th October 2004

What I Really Want to Say

Let’s Take the Word Intelligence Back from Bush

20th August 2004

Still Worth Reading

Big Media, Journalists and Politics

18th August 2004

What I Really Want to Say

The Iraqi Democracy That Hasn’t Happened

11th August 2004

What I Really Want to Say

Welcome to my Blog

8th August 2004

SF Gate

SF Gate 2002

Tech Futures Where workers and investors will find opportunities in the years ahead

7th November 2002

Harvard Business Publishing

Feedback in the Future Tense

1st November 2002

SF Gate

SF Gate 2002

Picture This Government Web sites are for the people not incumbent office-holders

24th October 2002

SF Gate

SF Gate 2002

Silicon Valley Fights Back Hollywood has a worthy adversary in South Bay Congresswoman Zoe Lofgren

9th October 2002

SF Gate

SF Gate 2002

Free Mickey Stanford Law Professor seeks to overturn the Sonny Bono Copyright Extension Act

26th September 2002

SF Gate

SF Gate 2002

Berman-Coble Goes Too Far Legalizing hacking of P2P networks hurts start-ups, not thieves

12th September 2002

SF Gate

SF Gate 2002

Open-Source Government Free-software guru Bruce Perens has a new information-technology solution

29th August 2002

SF Gate

SF Gate 2002

Take The Medicine By not expensing stock options now, tech firms are just prolonging the pain

15th August 2002

SF Gate

SF Gate 2002

Not a Moment Too Soon Digiportal’s innovative challenge response ChoiceMail program means the end of spam

30th July 2002

SF Gate

SF Gate 2002

The Disintermediation Blues On the sad state of online car- and mortgage-buying services

18th July 2002

SF Gate

SF Gate 2002

Taxing Workers Cutting capital gains taxes could hurt Silicon Valley in the long run

3rd July 2002

SF Gate

SF Gate 2002

Fuel Cell Hold-up Government’s go-slow approach promises to keep the technology on the shelf

20th June 2002

SF Gate

SF Gate 2002

Nanotechnology’s First Fruits Products nearing market promise to lead the budding industry from hype to reality

6th June 2002

SF Gate

SF Gate 2002

Ocean Rescue Planktos Foundation hopes to reduce global warming by fertilizing the seas

22nd May 2002

SF Gate

SF Gate 2002

Hollywood’s Way Out New distribution platform is solution for copyright theft

9th May 2002

SF Gate

SF Gate 2002

Shooting Blanks Growing digital rights movement needs to put some political heads on stakes — fast

22nd April 2002

SF Gate

SF Gate 2002

Sharing The Airwaves Spread spectrum technology could bring a new dawn for broadcasting

11th April 2002

Harvard Business Publishing

Is Risk the Cost of Innovation?

1st April 2002

SF Gate

SF Gate 2002

Cold Fusion Rides Again Science magazine publishes more evidence of tabletop nuclear reactions

25th March 2002

SF Gate

SF Gate 2002

Vexing Options Accounting scandal fallout could mean positive changes for workers and investors

25th February 2002

SF Gate

SF Gate 2002

All Hail Creative Commons Stanford professor and author Lawrence Lessig plans a legal insurrection

11th February 2002

SF Gate

SF Gate 2002

Search Me Doom ahead for search engines that charge listing fees

28th January 2002

SF Gate

SF Gate 2002

Political Weapons The missile defense shield will help neutralize the tech sector

17th January 2002

SF Gate

SF Gate 2001

Playing The Biotech Boom Picking biotech stocks is not a game for novices

31st December 2001

SF Gate

SF Gate 2001

The Westly Factor Why a usually obscure state election might matter most for tech firms

17th December 2001

SF Gate

SF Gate 2001

The “Last Mile” Problem ADCOs could finally bust open the local phone market

6th December 2001

SF Gate

SF Gate 2001

The End Of Hewlett-Packard As We Knew It? Revered company is between a rock and a hard place

19th November 2001

SF Gate

SF Gate 2001

War Boom More Pentagon spending could actually hurt Silicon Valley

23rd October 2001

SF Gate

SF Gate 2001

Energy Independence Now We Need A New Energy Revolution

4th October 2001

SF Gate

SF Gate 2001

No Silver Bullets Giving Up Privacy for Security Will Leave Us With Neither

18th September 2001

SF Gate

SF Gate 2001

Kick ‘Em When They’re Down Silicon Valley’s Usual CEO Excuses Don’t Tell the Real Story

23rd August 2001

SF Gate

SF Gate 2001

Slap the PUC It May Be the Last Chance to Protect Independent ISPs From Extinction

31st July 2001

CNBC

CNBC 2001

Will Webvan Group’s Stock Deliver?

23rd July 2001

CNBC

CNBC 2001

Sanmina Can’t Buy Demand

19th July 2001

CNBC

CNBC 2001

Fund Managers Say: Get Real!

13th July 2001

SF Gate

SF Gate 2001

The New Napster The Record Industry Has Met its Match

10th July 2001

CNBC

CNBC 2001

Analysts Predict i2 Comeback

9th July 2001

CNBC

CNBC 2001

Envision the Tech Rebound

6th July 2001

CNBC

CNBC 2001

Isis May Hit Psoriasis Pay Dirt

26th June 2001

CNBC

CNBC 2001

Oracle Under Pressure

22nd June 2001

SF Gate

SF Gate 2001

The Next Frontier The Tech Sector Needs A Nanotechnology Target

21st June 2001

CNBC

CNBC 2001

PeopleSoft Gaining on Oracle

19th June 2001

CNBC

CNBC 2001

3 Wireless Plays for 2002

18th June 2001

CNBC

CNBC 2001

Intel’s Visibility Only Half the Battle

8th June 2001

SF Gate

SF Gate 2001

Cisco’s Slide Tech Bellwether Must Find A New Path To Success

5th June 2001

CNBC

CNBC 2001

What’s Next for Microsoft?

30th May 2001

CNBC

CNBC 2001

Expedia, Travelocity Make the Cut

25th May 2001

CNBC

CNBC 2001

Agile’s CEO Speaks

24th May 2001

CNBC

CNBC 2001

TiVo’s Future in Question

22nd May 2001

CNBC

CNBC 2001

Is AMAT Ahead of Itself?

18th May 2001

CNBC

CNBC 2001

Uncertainty Lingers for Dell

17th May 2001

CNBC

CNBC 2001

Rambus on the Ropes

15th May 2001

SF Gate

SF Gate 2001

Free Higher Education MIT’s OpenCourseWare Plan Fires the First Real Shot

10th May 2001

CNBC

CNBC 2001

No Quick Cisco Fix

10th May 2001

CNBC

CNBC 2001

B2B Death Exaggerated

8th May 2001

CNBC

CNBC 2001

Exodus May Be at Crossroads

4th May 2001

CNBC

CNBC 2001

Siebel’s Challenges Grow

2nd May 2001

CNBC

CNBC 2001

Mr. Cisco Meet Mr. Avici

27th April 2001

CNBC

CNBC 2001

Ariba Answers Critics

25th April 2001

CNBC

CNBC 2001

A Value Manager Names Favorites

24th April 2001

SF Gate

SF Gate 2001

Desktop Linux Eazel Inc. Could Change the World Or Go Broke Trying

19th April 2001

CNBC

CNBC 2001

IBM Still Has Safety Net

18th April 2001

CNBC

CNBC 2001

A Potential Biotech Blockbuster

13th April 2001

CNBC

CNBC 2001

Worries Linger for Hewlett Packard

10th April 2001

CNBC

CNBC 2001

Will Sun Warn?

6th April 2001

CNBC

CNBC 2001

What’s Next for Yahoo!?

5th April 2001

SF Gate

SF Gate 2001

Timing The Tech Stock Recovery Investors Should Trust Themselves, Not The Analysts

4th April 2001

CNBC

CNBC 2001

Red Hat: Slow, Steady Progress

29th March 2001

CNBC

CNBC 2001

Oracle: Another Moment of Truth

27th March 2001

CNBC

CNBC 2001

Pick of the Week: Coca-Cola

26th March 2001

CNBC

CNBC 2001

Cisco: No Bargain Yet

22nd March 2001

CNBC

CNBC 2001

In Intel vs. AMD, Neither Wins

20th March 2001

CNBC

CNBC 2001

Analyst Pick: L-3 Communications

19th March 2001

CNBC

CNBC 2001

Can XP Invigorate Microsoft?

15th March 2001

SF Gate

SF Gate 2001

Buying The Grid Gov. Davis’ Plan Puts Taxpayers on the Wrong Side of Future Technologies

13th March 2001

CNBC

CNBC 2001

Valuing VeriSign

12th March 2001

CNBC

CNBC 2001

Some EMS Stocks May Bounce

8th March 2001

CNBC

CNBC 2001

Vignette CEO Counters Critics

6th March 2001

CNBC

CNBC 2001

A Sad Vignette

2nd March 2001

SF Gate

SF Gate 2001

ReplayTV vs. TiVo TiVo vs. ReplayTV

27th February 2001

CNBC

CNBC 2001

Straight Story on Align Tech

27th February 2001

CNBC

CNBC 2001

Bumpy Flight for Net Travel Stocks

26th February 2001

CNBC

CNBC 2001

Can Handspring Beat The Odds?

12th February 2001

CNBC

CNBC 2001

Webvan’s Days Appear Numbered

8th February 2001

CNBC

CNBC 2001

Akamai’s Stock Soars Again

30th January 2001

SF Gate

SF Gate 2001

Where’s The Competition? How California’s Leaders Helped Create the Energy Crisis

25th January 2001

CNBC

CNBC 2001

New Index May Move Biotechs

25th January 2001

CNBC

CNBC 2001

Can Stock Valuations Grow?

23rd January 2001

CNBC

CNBC 2001

Aether Systems Inc. Soars Again

22nd January 2001

CNBC

CNBC 2001

How IBM Beat Earnings Estimates

17th January 2001

CNBC

CNBC 2001

IPO Recovery Possible Next Year

2nd January 2001

CNBC

CNBC 2000

Contract Manufacturing: A Second-Half Bet (part 2)

28th December 2000

CNBC

CNBC 2000

No Security for Network Associates’ Shareholders

27th December 2000

SF Gate

SF Gate 2000

Machine Error The Case for Paper Ballots

21st December 2000

CNBC

CNBC 2000

Critical Months Ahead for Oracle

21st December 2000

CNBC

CNBC 2000

Symantec Charts New Course

19th December 2000

CNBC

CNBC 2000

Power Play: Fuel-Cell Stocks

18th December 2000

CNBC

CNBC 2000

Microsoft Warning No Surprise

14th December 2000

CNBC

CNBC 2000

Abgenix: The Mouse That Roars?

14th December 2000

CNBC

CNBC 2000

Will Linux Save Microsoft?

8th December 2000

CNBC

CNBC 2000

PC Group: Don’t Hold Your Breath

6th December 2000

CNBC

CNBC 2000

TiVo Winning Converts

1st December 2000

CNBC

CNBC 2000

Two Hot Net Technologies To Watch

22nd November 2000

SF Gate

SF Gate 2000

Technical Correction “The Numbers Guy” And Wall Street

21st November 2000

CNBC

CNBC 2000

Biopure on Verge of Biotech Holy Grail

16th November 2000

CNBC

CNBC 2000

Adobe Systems Corners Its Market

15th November 2000

CNBC

CNBC 2000

Sign of a Top: A VC Fund for Jocks

14th November 2000

CNBC

CNBC 2000

Is McAfee the Play in Anti-Virus Stocks?

10th November 2000

CNBC

CNBC 2000

Time to Sell Solectron, Buy SCI?

8th November 2000

CNBC

CNBC 2000

“Fiorina’s Folly” at Hewlett Packard

6th November 2000

CNBC

CNBC 2000

IBM Jilts Transmeta at IPO altar

2nd November 2000

CNBC

CNBC 2000

AVANT: A Biotech With Heart

1st November 2000

CNBC

CNBC 2000

Netegrity Inc. Is Coming on Strong

30th October 2000

CNBC

CNBC 2000

A Long Wait for the Wireless Web

26th October 2000

CNBC

CNBC 2000

Time to Bite at Apple’s Stock?

23rd October 2000

CNBC

CNBC 2000

Crime Pays for Online-Security Firms

19th October 2000

SF Gate

SF Gate 2000

Faster Than Light Travel Will We Ever Travel to the Stars?

18th October 2000

CNBC

CNBC 2000

Is Oracle’s E-Biz Presence Overstated?

17th October 2000

CNBC

CNBC 2000

UpShot Presents Problems for Oracle

17th October 2000

CNBC

CNBC 2000

Leading B2Bs May Be Heading for Fall

12th October 2000

CNBC

CNBC 2000

Transmeta’s Big-Bark, No-Bite IPO

11th October 2000

CNBC

CNBC 2000

Cashing in on the Optics Opportunity

5th October 2000

CNBC

CNBC 2000

Priceline Business Model Seen Flawed

3rd October 2000

CNBC

CNBC 2000

Little Thunder Seen for Loudcloud IPO

28th September 2000

CNBC

CNBC 2000

PC Sales May Pick up Later in the Year

22nd September 2000

SF Gate

SF Gate 2000

Burn Your Cubicle Virtual Teams Are the Future of Work

21st September 2000

CNBC

CNBC 2000

Analysts Talk Hot Biotech Stock Picks

14th September 2000

CNBC

CNBC 2000

Art Tech Seen as Buying Opportunity

13th September 2000

CNBC

CNBC 2000

Why Analysts Like Flextronics

11th September 2000

CNBC

CNBC 2000

Will the Holidays Be Kind to E-Tailers?

7th September 2000

CNBC

CNBC 2000

Analysts Like Ask Jeeves’ Prospects

6th September 2000

SF Gate

SF Gate 2000

Fast and Easy New Browserless Apps Allow One-Click Searching

31st August 2000

CNBC

CNBC 2000

Four VOIP Stock Favorites

31st August 2000

CNBC

CNBC 2000

Analysts Debate Merit of Free VOIP Telephone Calls

24th August 2000

CNBC

CNBC 2000

Analysts Set Higher Targets for CIENA

22nd August 2000

CNBC

CNBC 2000

Techs That Thrive in a Slowing Economy

21st August 2000

CNBC

CNBC 2000

Stalled Fuel Cell IPOs Leave Upside

15th August 2000

CNBC

CNBC 2000

Election Imperils New Economy Stocks

11th August 2000

CNBC

CNBC 2000

Obscure Tech Sector Poised for Growth

8th August 2000

CNBC

CNBC 2000

Analysts Say Plexus Hits Sweet Spot

2nd August 2000

SF Gate

SF Gate 2000

Little Man, Big Mind New Media Pioneer Gary Brickman’s Remarkable Life

31st July 2000

CNBC

CNBC 2000

Solectron Stock Set to Soar in 2nd Half

31st July 2000

CNBC

CNBC 2000

Will Webvan Group’s Stock Deliver?

25th July 2000

CNBC

CNBC 2000

InfoSpace Leads Next Wireless Trend

20th July 2000

CNBC

CNBC 2000

Analysts Say VISX’s Stock Looks Good

18th July 2000

CNBC

CNBC 2000

Analysts, CEO Talk Up MedicaLogic

10th July 2000

SF Gate

SF Gate 2000

Who Wants to be a Millionaire? Coming Up With the Next Big Thing

28th June 2000

CNBC

CNBC 2000

Intel Surges, But Some Risks Remain

21st June 2000

CNBC

CNBC 2000

Can Be Inc.’s Stock Make Comeback?

19th June 2000

CNBC

CNBC 2000

Electronic Mfg Group Seen as Good Bet

12th June 2000

SF Gate

SF Gate 2000

Talking Computers Microsoft’s Long-Range Plan to Thwart the Feds

7th June 2000

CNBC

CNBC 2000

Echelon Triples on Investor Enthusiasm

6th June 2000

CNBC

CNBC 2000

Microsoft: Seen Solid in Long-Term

1st June 2000

CNBC

CNBC 2000

Analysts Like Nortel As Tech Leader

31st May 2000

SF Gate

SF Gate 2000

Digital Food Online Groceries Set Stage for Long-Awaited Revolution in the Aisles

26th May 2000

CNBC

CNBC 2000

Hot Biotech Stocks for the Long Term

25th May 2000

CNBC

CNBC 2000

Hot Biotech Stocks for the Long Term

25th May 2000

CNBC

CNBC 2000

Symantec Finds Favor Among Analysts

24th May 2000

CNBC

CNBC 2000

Yahoo! Wireless, B2B Plans Get Raves

22nd May 2000

CNBC

CNBC 2000

IBeam IPO Makes Modest Debut

19th May 2000

CNBC

CNBC 2000

Cisco’s Margins Seen Under Pressure

15th May 2000

CNBC

CNBC 2000

FairMarket Business Model Seen as Solid

14th May 2000

CNBC

CNBC 2000

Digital Video Recorder Stocks Seen Up

11th May 2000

SF Gate

SF Gate 2000

Highway Robbery New electronic toll collection system won’t fix traffic woes

10th May 2000

CNBC

CNBC 2000

HomeGrocer IPO Makes Tepid Debut

10th May 2000

CNBC

CNBC 2000

Analysts Say Rambus Ride Not Over

8th May 2000

CNBC

CNBC 2000

Napster May Hurt Music-Firm Stocks

1st May 2000

CNBC

CNBC 2000

Future Seen Bright for Axent

1st May 2000

CNBC

CNBC 2000

Long-Term Trends Favor Foundries

27th April 2000

CNBC

CNBC 2000

Upside Seen for Silicon Valley Stock

26th April 2000

CNBC

CNBC 2000

Analysts See Liberate Stock Jumping

25th April 2000

CNBC

CNBC 2000

It’s Time for Dot-Com Bottom-Fishing

20th April 2000

CNBC

CNBC 2000

Higher Earnings Seen for PC Makers

13th April 2000

CNBC

CNBC 2000

Chip-Sector Earnings Look Strong

12th April 2000

CNBC

CNBC 2000

Saba Shares More Than Double

7th April 2000

CNBC

CNBC 2000

OPUS360 Shares Jump After IPO

7th April 2000

SF Gate

SF Gate 2000

Napster How free music will change the planet

6th April 2000

CNBC

CNBC 2000

Microsoft Woes May Boost Linux Firms

5th April 2000

CNBC

CNBC 2000

Some See Upside for Healtheon

4th April 2000

CNBC

CNBC 2000

ArrowPoint IPO Shoots Higher in Debut

31st March 2000

CNBC

CNBC 2000

Here Comes a Slew of Biotech IPOs

24th March 2000

CNBC

CNBC 2000

Sorting Through a Slew of Biotech IPOs

24th March 2000

CNBC

CNBC 2000

Blaze IPO Is a Flaming Success

23rd March 2000

CNBC

CNBC 2000

Caldera Systems IPO Soars in Debut

21st March 2000

SF Gate

SF Gate 2000

Patently False Time for Bezos to get serious

17th March 2000

CNBC

CNBC 2000

3 Potentially Hot ASP Stocks to Watch

17th March 2000

CNBC

CNBC 2000

Can Other ASPs Match Cobalt’s Success?

16th March 2000

CNBC

CNBC 2000

Analyst Pick: KEMET

12th March 2000

CNBC

CNBC 2000

Selectica IPO Leaps Higher on First Day

10th March 2000

CNBC

CNBC 2000

IPrint.com’s IPO Makes Weak Debut

8th March 2000

CNBC

CNBC 2000

Net2000 IPO Jumps in Opening Trading

7th March 2000

CNBC

CNBC 2000

Analysts Divided on Net Registrar Group

7th March 2000

CNBC

CNBC 2000

Analysts Cautious on Net Ad Stocks

29th February 2000

CNBC

CNBC 2000

Hotel Reservations IPO Opens Strongly

25th February 2000

SF Gate

SF Gate 2000

Deposit This On the Internet, your bank is not your friend

23rd February 2000

CNBC

CNBC 2000

Nextel Partners IPO Makes Solid Debut

23rd February 2000

CNBC

CNBC 2000

Webvan’s Survival Plan

21st February 2000

CNBC

CNBC 2000

Banks Face Threat from Financial Portals

18th February 2000

CNBC

CNBC 2000

Inforte IPO Rockets Higher in Debut

18th February 2000

CNBC

CNBC 2000

Apropos IPO Leaps up on Opening Day

17th February 2000

CNBC

CNBC 2000

Repeat Buyers Boost Eloquent Inc. IPO

17th February 2000

CNBC

CNBC 2000

Good Track Record Boosts Lante’s IPO

11th February 2000

CNBC

CNBC 2000

Pets.com IPO Makes Modest Debut

11th February 2000

CNBC

CNBC 2000

Rough Seas Seen for Health-Care B2Bs

10th February 2000

CNBC

CNBC 2000

Hacker Attacks Overshadow Buy.com IPO

9th February 2000

CNBC

CNBC 2000

Mediacom IPO Makes Modest Debut

4th February 2000

CNBC

CNBC 2000

Big E-Tail Enablers Seen as Best Long-Term Bets

4th February 2000

CNBC

CNBC 2000

Turnstone Business Model Drives up IPO

1st February 2000

CNBC

CNBC 2000

Sequenom IPO Shoots Higher in Debut

1st February 2000

CNBC

CNBC 2000

IPO Fever Continues with 724 Solutions

28th January 2000

CNBC

CNBC 2000

InterWAVE IPO Shines as Expected

28th January 2000

CNBC

CNBC 2000

Extensity IPO Gets Explosive Start

27th January 2000

CNBC

CNBC 2000

Neoforma.com Shares Soar in Debut

24th January 2000

CNBC

CNBC 2000

Smaller Chip Firms Seen as Value Plays

21st January 2000

CNBC

CNBC 2000

Internet Stocks for 2000, Part Two

17th January 2000

CNBC

CNBC 2000

Internet Stocks for 2000, Part One

17th January 2000

CNBC

CNBC 2000

Analyst Sees Onyx Software Doubling

14th January 2000

CNBC

CNBC 2000

Sonic Foundry Stock Seen Extending Run

7th January 2000

CNBC

CNBC 2000

Future Bright for Young DSL Companies

6th January 2000

SF Gate

SF Gate 2000

Open Source TV Broadcasters should jump on the open source bandwagon, pronto

5th January 2000

CNBC

CNBC 2000

MIPS’s Stock Seen Heading Back Up

3rd January 2000

CNBC

CNBC 2000

Don’t Count Cable Firms Out

2nd January 2000

CNBC

CNBC 2000

2000 Expected to Set New IPO Record

2nd January 2000

CNBC

CNBC 2000

Exodus’s Stock Seen Going Higher

1st January 2000

CNBC

CNBC 1999

Citrix Seen as Hot Stock for 2000

30th December 1999

CNBC

CNBC 1999

Caching Stocks Lead Internet Sector

26th December 1999

SF Gate

SF Gate 1999

Our Wacky Patent System And its perilous, toothless reform

23rd December 1999

CNBC

CNBC 1999

AltaVista IPO Seen Big, Despite Losses

21st December 1999

CNBC

CNBC 1999

Are the Linux Backers Right?

18th December 1999

CNBC

CNBC 1999

Maxygen Engineers Strong IPO Showing

16th December 1999

CNBC

CNBC 1999

Caliper IPO Tests Biotech Waters

15th December 1999

CNBC

CNBC 1999

IPO MedicaLogic Off to Good Start

12th December 1999

CNBC

CNBC 1999

VA Linux Tries to Overtake Red Hat

9th December 1999

CNBC

CNBC 1999

Preview Systems Jumps on First Day

8th December 1999

CNBC

CNBC 1999

NetRatings IPO Makes Strong Debut

8th December 1999

SF Gate

SF Gate 1999

Click Here To Buy Online shopping tips from someone who hates to shop

8th December 1999

CNBC

CNBC 1999

More Gains Seen for Keynote Systems

7th December 1999

CNBC

CNBC 1999

HealthCentral Takes Aim at Dr. Koop

7th December 1999

CNBC

CNBC 1999

New Issue Digimarc Opens Strongly

2nd December 1999

CNBC

CNBC 1999

McAfee Jumps on First Trading Day

2nd December 1999

CNBC

CNBC 1999

Web Site Offers Gurus’ Stock Picks

2nd December 1999

CNBC

CNBC 1999

WebTrends Seen Continuing to Rise

1st December 1999

SF Gate

SF Gate 1999

Readers’ Beat SF Gate column readers respond

24th November 1999

CNBC

CNBC 1999

Push into E-Commerce Seen Driving BEA

23rd November 1999

CNBC

CNBC 1999

CacheFlow Latest Red-Hot Net IPO

19th November 1999

CNBC

CNBC 1999

Investors Bid New Issue Imanage up Sharply

17th November 1999

CNBC

CNBC 1999

Quintus Corp. IPO Makes Strong Debut

16th November 1999

CNBC

CNBC 1999

Immersion Corp. Makes a Strong Debut

12th November 1999

SF Gate

SF Gate 1999

Going Once, Going Twice, Gone! eBay is shooting itself in the foot

11th November 1999

CNBC

CNBC 1999

One Step Ahead: Tech Funds Give the Scoop

11th November 1999

CNBC

CNBC 1999

Expedia IPO Takes Off Strongly

10th November 1999

CNBC

CNBC 1999

Cobalt Hits It Big on Debut

5th November 1999

CNBC

CNBC 1999

Webvan Hits Market As Expected

5th November 1999

CNBC

CNBC 1999

One Step Ahead: More Health-Care IPOs?

4th November 1999

CNBC

CNBC 1999

Analysts Say Puma’s Best Days Are Ahead

1st November 1999

CNBC

CNBC 1999

IPO Pipeline: Content + Commerce = How2

29th October 1999

SF Gate

SF Gate 1999

Big Idiot on Campus UC should broadcast class lectures online

28th October 1999

CNBC

CNBC 1999

Investors Curious About XML Bandwagon

25th October 1999

CNBC

CNBC 1999

CV Therapeutics: A Heart-Stopping Stock

21st October 1999

CNBC

CNBC 1999

Transactions Put CyberSource in Driver’s Seat

19th October 1999

SF Gate

SF Gate 1999

Open Sesame How Collab.net takes open-source to the next level

14th October 1999

CNBC

CNBC 1999

E-Stamp and Stamps.com to Duke It Out

14th October 1999

CNBC

CNBC 1999

Is Healtheon a Buying Opportunity?

13th October 1999

CNBC

CNBC 1999

Will the Palm Pilot IPO Lift 3Com’s Stock?

12th October 1999

CNBC

CNBC 1999

Personal Touch Pays Off for Art Technology

5th October 1999

CNBC

CNBC 1999

IPO Pipeline: Immersion Set for This Week

4th October 1999

CNBC

CNBC 1999

TiVo Soars But Challenges Remain

1st October 1999

SF Gate

SF Gate 1999

The Great Tech Showdown I’m rooting for Bill Gates

30th September 1999

CNBC

CNBC 1999

The Server Boom, Part II: Cobalt Plans IPO

30th September 1999

CNBC

CNBC 1999

Cashing in on the Coming Server Boom

29th September 1999

CNBC

CNBC 1999

Getting Back to Business in Taiwan

24th September 1999

CNBC

CNBC 1999

Who Is Next After Kana and eGain?

23rd September 1999

CNBC

CNBC 1999

ExpressDoctors Combines House Calls and the Net

20th September 1999

CNBC

CNBC 1999

Searchbutton.com Sees Profit Before IPO

18th September 1999

SF Gate

SF Gate 1999

The Kids Are Not Alright Why Johnny can’t compute

15th September 1999

CNBC

CNBC 1999

Wink Stock Outruns Company Performance

15th September 1999

CNBC

CNBC 1999

Start-Up Collab.Net Hopes to Follow Red Hat’s Example

14th September 1999

CNBC

CNBC 1999

Epinions.com Aims to Change Online Shopping

13th September 1999

CNBC

CNBC 1999

Netro Soars on Broadband-Wireless Hopes

11th September 1999

CNBC

CNBC 1999

AOL Gives Preview Travel Its Money’s Worth

9th September 1999

CNBC

CNBC 1999

Beam Me up Some Cash

8th September 1999

CNBC

CNBC 1999

Picking the Right Internet Stocks

7th September 1999

CNBC

CNBC 1999

Agile Software Succeeds by Design

3rd September 1999

CNBC

CNBC 1999

Apple’s New TV Campaign Targets Intel

2nd September 1999

Harvard Business Publishing

Nine-Step Guide to Fast, Effective Business Writing

1st September 1999

SF Gate

SF Gate 1999

Masters of Our Domain RealNames means just what the name says

31st August 1999

CNBC

CNBC 1999

To Be or Not to Be?

31st August 1999

CNBC

CNBC 1999

So, You Want to Be an Angel Investor?

30th August 1999

CNBC

CNBC 1999

Mypoints.com Builds Loyalty and Value

27th August 1999

CNBC

CNBC 1999

Need for Speed Sends Two Stocks Soaring

26th August 1999

CNBC

CNBC 1999

Corel Rides Linux Bandwagon

24th August 1999

CNBC

CNBC 1999

Potholes on the Information Highway

23rd August 1999

CNBC

CNBC 1999

Solectron Shines in Outsourcing Sector

20th August 1999

CNBC

CNBC 1999

Two Net Companies Test Soft IPO Market

19th August 1999

CNBC

CNBC 1999

Sun’s Magic Is Its Servers

18th August 1999

SF Gate

SF Gate 1999

Beta This Cleaning up the software industry’s bug-infested nest

17th August 1999

CNBC

CNBC 1999

Best Is Ahead for Applied Materials

17th August 1999

CNBC

CNBC 1999

Couch Potatoes Shun Quokka

13th August 1999

CNBC

CNBC 1999

Grove Latest to Tout Linux

11th August 1999

CNBC

CNBC 1999

Future Looks Bright for Web Sites Targeted at Women

10th August 1999

CNBC

CNBC 1999

Tellme Networks Isn’t Saying Much

6th August 1999

CNBC

CNBC 1999

Investor Optimism Leaves Some Worried

6th August 1999

CNBC

CNBC 1999

New Buyer Services Pose Threat to Online Retailers

5th August 1999

SF Gate

SF Gate 1999

Running Lame Most presidential candidates stumble online

4th August 1999

CNBC

CNBC 1999

Yahoo! Struggles With Its Valuation

3rd August 1999

CNBC

CNBC 1999

Venture Investments Up, But Returns Trend Downward

2nd August 1999

Harvard Business Publishing

Automated E-mail Response: What Managers Need to Know

1st August 1999

CNBC

CNBC 1999

Hewlett Packard Pulls Out the Stops

30th July 1999

CNBC

CNBC 1999

The Mouse Business Is Roaring

29th July 1999

CNBC

CNBC 1999

FCC Gives Boost to AT&T’s High-Speed Hopes

28th July 1999

CNBC

CNBC 1999

Pending Red Hat IPO Boosts Server Market

27th July 1999

CNBC

CNBC 1999

E-Mail Responders Get Ready for IPOs

23rd July 1999

CNBC

CNBC 1999

Third-Party Software, International Sales To Determine Apple’s Future

21st July 1999

SF Gate

SF Gate 1999

Killing Uncle Sam The taxman meets his match online

20th July 1999

SF Gate

SF Gate 1999

Wanna Make a Bet? How the ‘Net can improve your odds

6th July 1999

SF Gate

SF Gate 1999

We’re Flying Blind Time for New Economic Metrics

22nd June 1999

SF Gate

SF Gate 1999

Tech Stocks Has the boom gone bust?

9th June 1999

Harvard Business Publishing

Six Sigma: What It Is and How to Use It

1st June 1999

SF Gate

SF Gate 1999

Must See TV Get paid to watch

25th May 1999

SF Gate

SF Gate 1999

The War Against Cold Fusion What’s really behind it?

17th May 1999

Harvard Business Publishing

How to Communicate with Telecommuters

1st May 1999

SF Gate

SF Gate 1999

Oh Holy Net Does the Hand of God Know HTML?

28th April 1999

SF Gate

SF Gate 1999

Love Bytes Will the Net flatten Maslow’s pyramid?

12th April 1999

SF Gate

SF Gate 1999

Killing the Rainmakers The dying art of high-tech public relations

29th March 1999

SF Gate

SF Gate 1999

Power To The People The return of cold fusion

15th March 1999

1

2