Will Sun Warn?

Will Sun Warn?

By Hal Plotkin

CNBC.com Silicon Valley Correspondent

Apr 6, 2001 03:57 PM

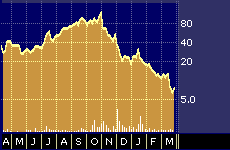

JNI Corp. 52-week stock performance

Sun Microsystems Inc. supplier JNI Corp.’s recent earnings warning has led to speculation in several quarters that Sun might follow suit with an earnings warning of its own prior to the company’s formal announcement of its third quarter results scheduled for Thursday, April 19.

Earlier this week, Goldman Sachs analyst Laura Conigliaro publicly suggested that Sun {SUNW} could be among the companies issuing earnings warnings over the next few days. The analyst cited the “ugly” situation for enterprise systems companies, which she said could lead to additional downside risk to Sun’s shares of 10 to 30 percent.

Conigliaro’s warning came on the heels of a report published one week earlier from Silicon Valley-based Zona Research that said JNI’s {JNIC} recent warning was an ominous sign for Sun shareholders.

“We view JNI’s warning of revenue shortfalls as a bellwether of coming events at Sun, as JNI, which makes adapters for Sun’s storage networks, attributed its own shortfall to weakness in Sun’s server market,” the Zona report concluded.

Late last month, JNI said it expects fiscal first quarter revenues to rise 9 to 12 percent to $20 to $21 million from the $18.5 million the company posted a year earlier, with net income, excluding amortization, of 3 cents to 4 cents a share, compared with 8 cents for the same period one year earlier. JNI’s more optimistic January forecast had indicated that first half revenues could rise 40 percent to 50 percent year over year, with earnings for the full fiscal 2001 year coming in somewhere between 80 cents to 85 cents a share.

“With the majority of our revenues derived from sales of Sun Solaris-based products, continued weakness in the Sun server marketplace has had an impact on first quarter performance,” said Neal Waddington, JNI’s president and chief executive officer, in a statement that accompanied the lowered guidance.

A Sun spokesperson refused to comment on the rumors of an imminent earnings warning, but also indicated there would be no additional announcements from the company prior to its official earnings report.

“Our corporate policy is not to confirm or deny rumors, so I can’t help you out with that question,” wrote Sun spokesperson Elizabeth McNichols in an email response to CNBC.com. “We are currently in our quiet period before the earnings announcement on April 19, so we cannot provide any further comments on outlook until that time,” she added.

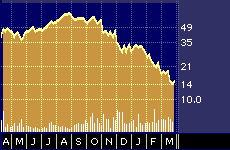

Sun Microsystems 52-week stock performance

Conigliaro, of Goldman Sachs, did not return CNBC.com’s call seeking an interview. Sun’s last public comment on earnings came in late February, when the company shaved sequential revenue expectations by 12 to 14 percent from the prior quarter and projected earnings per share in the seven to nine cent range. Sun posted earnings of 16 cents a share for its second quarter ended December 31, 2000.

Speculation about Sun missing its numbers is another indication of the significant slowdown that has hit many leading Silicon Valley tech firms. Prior to the recent disappointment Sun had met or beat analyst consensus expectations for 27 out of the last 28 quarters, according to Toni Sacconaghi, an analyst at Sanford C. Bernstein & Company, based in New York.

“I think a warning from Sun is pretty unlikely,” says Sacconaghi. “There really isn’t any history of warnings from the company. So I think if the news is sad, it’s going to come out in the [earnings] call.”

Sacconaghi currently has a “market perform” rating on the stock, adding that Sun, which still leads the high-end server market with approximately 40 percent market share, has become a victim of its own success. (Other players in or seeking to enter Sun’s market include Hewlett Packard Company {HWP}, International Business Machines Corp. {IBM}, Compaq Computer Corp. {CPQ}, Silicon Graphics Inc. {SGI}, and Dell Computer Corp. {DELL})

“Sun benefited enormously last year, but it set up some pretty difficult year-over-year comparisons,” says Sacconaghi. “It’s unclear to me that the stock has bottomed and neither the earnings nor the forward guidance will be particularly encouraging. We need to get a sense that the worst is fully visible, and we’re not there yet.”

S.G. Cowen analyst Richard Chu, based in Boston, agrees.

“Our guess is that business conditions are proving to be even more challenging than thought just a month ago,” Chu wrote in a research note published last week. “We think there is more downside to our near-term profit and loss assumptions for the fourth quarter and even to our below consensus assumptions for fiscal 2002, and certainly the first half [of 2002]. We see risk to both top line revenue and gross margins.”

Sun’s current difficulties stem primarily from weakness in the overall economy as well as its role as the leading supplier of UNIX servers, which are often used as the hub of internal corporate networks and Internet web sites. Dying dot coms and a general retrenchment in information technology spending has pulled the slats out from under the company’s growth story.

“It could be as much as 10 percent of their market is just gone,” says Joe Butt, an analyst at Forrester Research, based in Cambridge, Massachusetts. “My guess is that Sun will continue to remain as number one in the UNIX server market, at least for a while, but how the company does now depends a lot on what happens to e-business.”

Butt says that despite adverse macro-economic conditions over the short-term, he remains bullish on the company’s long-term future, particularly in the high-end server market where individual machines containing up to 64 microprocessors working in parallel can retail for upwards of $1 million dollars each.

“They’re getting more competition on the low end these days, particularly from Dell,” he says. “But there are more barriers to entry on the high end. You have to build the machines and then prove they can run in a reliable manner. That’s not something those running big data centers like to take a chance on. Which is why you see Sun servers in so many of those environments. I can’t say how the stock market will react. But I do think Sun will continue to do fine in the real market, particularly on the high end.”

Sacconaghi, at Sanford C. Bernstein & Company, also thinks Sun’s fairly safe in the high-end of the server market, which he says should grow at about 8 to 10 percent over the next five years, assuming the economy doesn’t fall into a recession.

“We think Sun continues to gain share in that market,” he says, adding that once the current malaise subsides there is no reason the company should not be able to grow revenues by about 15 percent a year and increase earnings by about 20 percent a year.

“But if information technology spending continues to be weak it’s going to affect everything,” he warns.