Worries Linger for Hewlett Packard

Worries Linger for Hewlett Packard

By Hal Plotkin

CNBC.com Silicon Valley Correspondent

Apr 10, 2001 04:16 PM

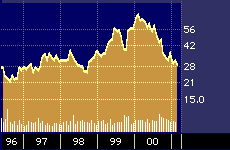

Hewlett Packard 5-year stock performance

Several tech stock specialists say they don’t expect to see a sustained recovery in Hewlett Packard Company’s {HWP} stock until sometime next year because of sluggish PC demand, tough competition in the UNIX server market, and growing signs of weakness in the company’s key foreign markets.

“Hewlett Packard is facing some serious issues for at least the next three to six months,” says Ian Link, portfolio manager of the Franklin Technology Fund. {FTCAX} “They had all their ducks in a row for 2001, so when the slowdown hit, it them particularly hard.”

Link says 2002 could be a better year for Hewlett Packard investors. But in the meantime, he says a significant recovery in shareholder value seems unlikely despite the company’s robust printer and related consumables business. There’s some disagreement on that point, although most of the analysts following the stock seem to side with Link.

Hewlett Packard tentatively plans to report its fiscal second quarter results on May 16.

“The reason people buy the stock is the annuity from the consumables business,” says Daniel Kunstler, an analyst at J. P. Morgan, based in San Francisco. “But the printer business as a franchise does not do quite as well in a down economy. We think the stock is at fair value now, without a lot of upside,” he warns.

Kunstler currently has a neutral “market perform” rating on the stock. All told, only two of the 21 analysts following Hewlett Packard now rate it a “strong buy,” which is virtually unchanged from three months ago. The continuing lack of enthusiasm from analysts reflects well-known concerns about troublesome macro-economic conditions for information technology vendors, as well as some more company-specific factors.

Late last month, for example, company CEO Carly Fiorina warned of an increasingly suspect climate in overseas markets, where Hewlett Packard currently generates about 61 percent of its revenues.

The warning led several analysts to cut revenue and earnings expectations for the firm. At the same time, some of them still contend that Hewlett Packard’s printer and printer supplies franchise provides it with something of an earnings floor, one that is not enjoyed by many of its competitors in the personal computer, computer server, and computer services businesses.

“Even though the difficult global economic conditions may impact at the margin, the prospects look favorable for HP’s imaging and printing supplies business to grow in the mid-teens, give or take a little, this year,” says a somewhat contrarian Richard Chu, an analyst at S. G. Cowen, in a recent report. In the same report, he shaved his earnings and revenue targets for HP, but also reiterated his “buy” recommendation and $40 12-month price target.

Chu now estimates that HP will post earning per share of $1.45 in fiscal 2001, down from his previous estimate of $1.58, and $1.75 in fiscal 2002, down from $1.85. On the optimistic side, however, he notes that HP’s high-margin consumables business, which accounts for the majority of its profits, grew at 16 percent during the January quarter, a time period when very few tech firms posted much if anything in the way of growth.

Chu says HP’s printer and consumables business, taken alone, should be worth about $28 to $30 a share, or roughly 23 to 25 times the $1.10 calendar year 2001 earnings per share that he expects will be generated by sales of printers and supplies.

Steve Koenig, senior analyst at market research firm NPD Intelect, says optimism about HP’s printer business seems justified given recent trends. In February, for example, the lastest period for which figures are available, HP managed to hold on to its lion’s share of the printer market, capturing about 53 percent of total in-store sales. The company’s closest competitor, Lexmark International Group Inc. {LXK}, came in a distant second, with 18.5 percent share.

Koenig adds that he expects to see more competition, particularly on price, coming from HP’s many rivals, which also include Seiko Epson Corporation’s U.S. affiliate, Epson America, Inc., Canon Inc. {CANNY} and Brother Industries Ltd. {BIL}. In particular, he says many of these major printer manufacturers are likely to begin lowering the costs of their ink cartridge refills and will also make it easier and less expensive for the owners of color printers to purchase refills of just the color they need, rather than be forced to purchase more costly multi-color cartridges.

“Cutting costs on the consumables is going to be the card some of these company’s will play,” Koenig predicts. “That’s a battlefront they are going to be shelling pretty hard.”

Ironically, though, Koenig says the cost cutting on consumables will probably end up helping rather than hurting Hewlett Packard in the long run because HP has the largest installed base of printers.

“When you give consumers more choice it makes them happier and it encourages them to print more,” Koenig says. The high cost of printing supplies, particularly for high-quality printers, discourages their use, he says. Cheaper ink should drive up sales and encourage more use of higher margin photo-quality printers.

“I don’t see HP as in jeopardy of losing their position in the printer market anytime over the next year,” he says. “I think we’ll see HP do whatever they have to do to protect their position.”

Link, at the Franklin Tech Fund, agrees that HP’s printer business and other diversified offerings put the company in a good position to tap a variety of interlocking markets once the growth of demand resumes. But he says that the current economic climate will put increasing pressure on all of HP’s other product segments, particularly personal computers and computer servers, which could continue to drag down earnings even if the printer business stays strong.

“Generally speaking, these stocks tend to start trading up three to six months ahead of the actual earnings trough,” Link says. “The problem is that trough could still be nine or more months ahead.”

Link says he is watching the situation very closely, and would scoop up the stock if it falls to a bargain 13 or 14 times this year’s earnings, which would put it at around $20 to $21 a share.

“At that price it would look quite attractive,” he says. “The other catalyst would be signs of a macro-economic bottom, but we’re not seeing that yet.”