A Value Manager Names Favorites

A Value Manager Names Favorites

By Hal Plotkin

CNBC.com Silicon Valley Correspondent

Apr 24, 2001 07:30 AM

Successful value investing is all about buying the right stocks and then waiting for the right time to come along, says Bruce Baughman, portfolio manager of the $1.2 billion dollar Franklin Balance Sheet Fund {FRBSX}.

Baughman’s fund, which adheres to a strict value-based investment discipline, was up 20.5 percent in 2000, outpacing the S&P 500 by nearly 30 percent over the same time period.

The fund’s performance was helped last year by little-known names such as Overseas Shipholding Group Inc. {OSG}. But Baughman says almost equally obscure American National Insurance Company’s {ANAT} stock is the better bet at the moment. Baughman’s fund currently owns both stocks.

“Our ideal stock is one that is selling under book value despite posting consistent earnings growth,” he says. “We may not always find exactly that. But in general we’re looking to get into situations where there is enough money left to compensate shareholders adequately even if the company involved has to sell off everything it owns and pay off all its debts.”

Actual corporate liquidations of that sort occur only rarely. But Baughman says using the book value yardstick as a stock-picking methodology is the best way to surface good investment opportunities that others have overlooked.

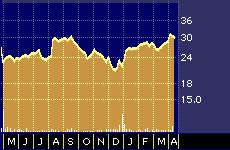

Overseas Shipholding Group 52-week stock performance

Overseas Shipholding Group Inc. was a case in point, says Baughman.

Baughman’s fund bought the stock last year at an average share price of around $17. What attracted him was a low P/E in a leading company in what was an out of favor group at the time. The company, which is based in New York, operates one of the largest and most modern crude oil tanker fleets in the world. Baughman took one look at the firm’s balance sheet, calculated the firm’s hard asset value, and decided the time to buy the company’s stock was when no one else wanted it. The value of the company’s ships alone, he says, made the stock a smart buy.

“No one wanted the oil price sensitive stocks when oil prices were low,” he says. “But we knew that was temporary and that it would go back up.” Tanker firms, and particularly firms with modern double-hulled tankers, do exceptionally well when oil prices are high because the tankers are usually kept running a full capacity.

Baughman’s holding on to his Overseas Shipholding Group stock and says he thinks the stock will continue to rise. But given its appreciation over the past year he says American National Insurance, which he also owns, provides investors with more certain appreciation potential over the next few years.

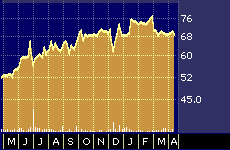

American National Insurance Company 52-week stock performance

Baughman calculates that Galveston, Texas-based American National Insurance’s stock is now selling at around 60 percent of book value. The company, which was founded in 1905, offers life, health, personal property, casualty, credit, annuities, and other types of insurance in both the US and Western Europe.

Baughman says he likes the fact that the company’s management is sometimes criticized for allegedly being too conservative, with some analysts saying the firm appears under-leveraged for a business with a $2 billion dollar market capitalization.

The flip side of that, he says, is the fact that the company’s stick-to-the-knitting philosophy, which is tied to its legacy of management by the members of one prominent Texas family, has led to 25 consecutive years of increased dividends.

Baughman says investors probably won’t need a catalyst of the sort that sent the oil stocks soaring to make an investment in American National Insurance pay off.

“The catalyst is the price,” he says. “I’ve seen the stock trading at or near book value in the past.”

Baughman says investors who want to understand the value methodology should study American National Insurance’s stock very closely. It’s an example, he says, of finding an opportunity to be paid to wait.

“They keep increasing their dividends, it’s a profitable company, and given how long it’s been around it’s likely they have assets that are not fully reflected in the book value, which is already quite attractive.”

Although he isn’t counting on it, Baughman says there is also always the chance that the family that runs the firm will eventually decide the time has come to cash out and sell the operation to some larger insurance or financial services firm.

“I’m happy with things going along there as they are,” he says. “But I’m preparing myself to be lucky.”

Baughman adds that thinking ahead of the herd has always been the key to successful value investing. That means avoiding the stocks everyone is talking about during periods when they are being pushed up to unsustainably high valuations. It sometimes takes a while for the market to return to its senses, he says, but periodic flights to quality are all but certain.

“I believe in the old saying that in the short run the market is a voting machine, but in the long run it’s a weighing machine.”

In the end, he says, the only thing that really matters is corporate performance.

Guide to Car Insurance Websites and Auto Insurance Web Sites

Hal’s Guide to Investment Web Sites

Term Life Insurance

Webhosting