Bumpy Flight for Net Travel Stocks

Bumpy Flight for Net Travel Stocks

By Hal Plotkin

CNBC.com Silicon Valley Correspondent

Feb 26, 2001 09:30 AM

Dot-com investors have learned some painful lessons over the past year about the limitations of the Internet, particularly when it comes to selling bulky items like pet food and groceries. That’s why many observers predict a far better future for companies such as Expedia Inc. {EXPE} and Travelocity.com Inc. {TVLY}, sellers of airline tickets and other travel-related reservations that can be both sold and delivered online.

Several financial analysts recently have set higher 12-month price targets on both stocks, saying they are exemplars of an online business model that can actually work. But a number of leading industry analysts who don’t make markets in stocks caution that the online travel area remains unsettled and that investors could be in for a big letdown if they think the sector’s two largest players have the whole thing sown up at this still-early stage of the game.

There have been several conspicuous flops in the online travel market, most notably Priceline.com Inc. {PCLN}. But the consensus among analysts is that Priceline’s woes were mostly of its own making. In particular, they blame Priceline’s unique “name your own price” marketing strategy, which didn’t allow customers to pick flight times or, often, even specific destinations. Firms selling airline tickets online in a more conventional way, such as Expedia and Travelocity, are typically portrayed as much safer bets.

The theory among their boosters is that Expedia, Travelocity and some of their peers are playing to the true strength of the Internet: the ability to sell “digital goods” that don’t require expensive warehouses, packing and shipping operations or costly procedures for dealing with returned items.

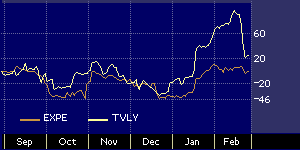

Expedia and Travelocity 6-month stock performance comparisons

That may explain why Expedia and Travelocity’s stocks have posted a better performance lately than most other dot-coms. Both have sold off in the past week after significant rallies, but analysts are sticking by sunny appraisals of their shares.

Their charts may not look pretty. But appearances aside, Expedia and Travelocity are two of the 10 dot-com merchants with market capitalization of more than $200 million whose stocks are currently trading closest to their 52-week highs. The leading online travel agency stocks showed more signs of life early this year than most other dot-com issues, shooting up 33 percent as a group in January, for example, a month when the Nasdaq recovered at a much slower 13-percent pace.

“Travel is a truly virtual product,” says Paul Keung, an analyst at CIBC World Markets, based in New York. “We’ve seen a pullback and consolidation in the space that benefits the two major players.”

In late January, Keung upgraded Travelocity’s stock to “strong buy” and reiterated the same rating on Expedia’s stock, setting 12-month price targets of 26 and 20, respectively.

Most other financial analysts tracking the stocks share the enthusiasm.

“We’re very positive on both names,” says Robert Lafleur, an analyst with Bear Stearns, based in New York. Lafleur has “buy” ratings, his firm’s highest recommendation, on both stocks. The Bear Stearns analyst doesn’t set specific price targets, but he says his firm’s buy recommendation implies 20 percent or more upside potential over the next year.

Backers of the leading online travel agency stocks don’t agree, however, on which of the two firms is the better play at the moment.

Some say that Travelocity, which currently ranks as the eighth-biggest seller of travel bookings in the United States, is better positioned given the firm’s many marketing partnerships with popular online portals, such as AOL {AOL}, Yahoo! {YHOO}, Lycos and Excite. AOL, for example, saw its travel bookings increase 48 percent in the nine months since it inked its revenue-sharing deal with Travelocity.

“Travelocity has the better marketing partnerships,” says Bailey Dalton, an analyst at C.E. Unterberg, Towbin, based in New York, who has a 12-month price target of 25 on Travelocity’s stock.

Expedia’s backers, on the other hand, prefer that company’s business plan, which relies more heavily on buying tickets in bulk at discount prices and then reselling them at higher margins than Travelocity. Travelocity derives revenue from thinner commissions that often top out at just $10 a ticket.

Expedia, now the ninth-largest seller of travel bookings in the United States, is a spin-off from Microsoft {MSFT} and is the preferred travel supplier on MSN, the software giant’s Web portal.

“Expedia’s approach means they understand the limitations of the commission model and are doing something to address that,” says Heidi Kim, travel analyst at New York-based Jupiter Media Metrix, a research firm that tracks online businesses.

The one big caveat, however, is the almost certain prospect of more competition for both Expedia and Travelocity moving forward. The major airlines are expected to roll out their own combined online ticketing site, called Orbitz, in June, assuming no interference from federal authorities on anti-trust grounds, which seems increasingly unlikely given the stated views of the current administration.

Even more troublesome, though, are indications that the most sophisticated online consumers are beginning to use online travel agencies to comparison shop before heading to the Web sites of the individual airlines, where they can often find better deals.

“There’s a big power struggle going on online,” says Kim, of Jupiter Media Metrix. “And at the end of the day, travel agencies are just middle men.”

Kim says there is about a 50-50 split right now between agencies and airlines when it comes to airline ticket sales. But going forward, she says she expects to see the individual airlines gain share against the agencies.

David Schehr, research director at Gartner, based in Stamford, Connecticut, agrees.

“People tend to be more loyal to airlines than agencies,” he says. “There’s this vague feeling that consumers have, especially when it comes to electronic [paperless] tickets, that they would rather be dealing directly with the airline.”

After the completion of the recent spate of mergers, three airlines will control about 75 percent of U.S. routes, so consumers will be able to comparison shop almost the entire country at three Web sites.

Schehr says he’s pretty sure the two leading online travel agencies will survive. But he adds that they’ll have to find more ways to add value and boost margins, such as through packaged vacation deals, to remain viable businesses.

“There’s really not that much of a value proposition selling tickets online as opposed to, say, buying them from an 800 number,” says Schehr. “Either way, you still have to go to the airport and get on the plane. And consumers are already figuring out that they can compare agency prices at the airline Web sites with just another two or three mouse clicks. And if they do that, they’re going to go for the lowest prices. After all, it’s the same plane.”

“The consumer demand for these products is real,” adds Kim, of Jupiter Media Metrix. “But there are several key elements needed to make sure the [online] agencies will be able to hold onto their customers and attract new ones.”

Few analysts doubt that the Internet will eventually become a dominant channel for airline ticket sales. But at least some of them say there are still some real questions about who will be left standing in that channel once the dust clears.

“None of the agencies are anywhere close to solving all the problems they are facing in terms of holding on to customers yet,” says Kim. “2001 will be the year we find out which ones will survive.”