Cisco: No Bargain Yet

Cisco: No Bargain Yet

By Hal Plotkin

CNBC.com Silicon Valley Correspondent

Mar 22, 2001 02:32 PM

Despite the carnage of recent months, several value fund managers say Cisco Systems Inc.’s {CSCO} stock still has to fall another 50 percent or so from its current level before it would begin to attract meaningful attention from bargain hunters in the mutual fund business.

That will undoubtedly come as unwelcome news to anyone currently holding Cisco shares. But it’s an essential piece of information for any would-be new Cisco investors who might think they’ve spotted a buying opportunity in Cisco’s beaten-down stock, which is now down a startling 75 percent from its 52-week high of $82 a share.

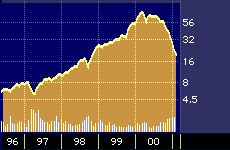

Cisco Systems 5-year stock performance

“I would still not say the stock is cheap by any means,” says Timothy Ghriskey, portfolio manager of the $105 million Dreyfus Aggressive Value {DAGVX} fund. “Even at these levels the stock is still trading at more than 30 times next year’s expected earnings, which is still well above the market.”

In early 2000, the overall U.S. stock market briefly traded at almost 40 times profits, which was roughly three times the average from 1946 to 1996. The recent stock market tumble, however, has pushed that number back down closer to the historical average.

That’s one of the main reasons why Ghriskey says Cisco’s stock won’t get much if any support from the value fund managers who have received the lion’s share of new mutual fund investments in recent weeks.

Bill Lippman, president of the $85 million Franklin Value Fund {FRVLX}, agrees. “We almost never buy a stock trading at 30 times earnings,” he says. “It would be a very rare occasion where we’d ever do something like that.”

On the surface, it might appear that Cisco’s stock has nonetheless been getting some support from securities analysts over the past few months. For example, the number of analysts giving the stock a “moderate buy” now totals 19, up from 10 three months ago.

But that’s only part of the picture – and likely misleading. If you dig a little deeper, you realize that most of those “moderate buy” ratings actually represent downgrades. Overall, the number of “strong buy” ratings on the stock has fallen from 26 three months ago to just 12 today. The downgrades to “moderate buy” are seen within the industry as a proxy for a “sell” rating, in part, because analysts are reluctant to slap a sell rating on a firm they might hope to do business with in the future.

“When it comes to Cisco, I’m telling investors to stay on the sidelines,” says Paul Segawa, an analyst at Bernstein Investment Research, based in New York.

Segawa is one of the few securities analysts to actually recommend selling a stock, in his case, Telefonaktiebolaget LM Ericsson {ERICY}, which he recommended dumping before its most recent slide began last September. He says he got close to putting a sell rating on Cisco a few weeks ago, but held back, in favor of his current hold rating.

On the optimistic side, Segawa says Cisco’s stock could be worth somewhere in the $25 to $30 range, but only if the company posts revenue growth of about 17 percent year-over-year for the next decade. He says that could happen. But he quickly adds that most estimates for the growth rate for telecom equipment purchases are coming in around 10 percent per year over the next few years, which would put even more pressure on the enterprise side of Cisco’s business.

You throw into that the law of large numbers, and Segawa grows even more concerned. Cisco posted $23.9 billion in revenue last year, which means the company would have to add close to $4 billion in new sales next year to achieve the projected growth rate required to justify a higher stock price.

While Cisco has posted revenue increases of more than 20 percent per year for the last 10 years, Sagawa says it’s “quite likely Cisco will see that streak stop now.”

Sagawa notes that in the entire history of the stock market there has only been one stock, International Business Machines Corporation {IBM} during the late 1950’s and 1960’s, that ever posted more than 20 percent year-over-year revenue growth for more than 15 years.

“It’s more than unusual to see that kind of sustained growth,” he says.

Martin Pyykkonen, an analyst at C. E. Unterberg, Towbin, based in San Francisco, is also among the legion of analysts once positive on Cisco’s stock but who now recommends a far more cautious approach.

“As far as loading up the truck to buy the stock at these levels I’d have to tell people to wait,” he says. “We need more visibility on the business, and there are still some issues that need to be worked out.”

Cisco generates about 40 percent of its revenue from customers in the hard-pressed telecommunications, or carrier, market, Pyykkonen notes, and the remaining 60 percent from the enterprise, or corporate customer, side.

“We’ll have to see the carrier market come back,” he says. “And the enterprise market also looks less attractive right now because of the economic slowdown. Those are the swing factors for Cisco’s top and bottom line revenue growth and we don’t know where they’re going yet.”

“Buying Cisco’s stock right now because the price is low is just as misguided as a year ago when people said the stock’s high price didn’t matter,” adds value fund manager Ghriskey. “The price does matter, but it has to be relative to something else.”

That “something else,” he says, the other critical factors to assess when looking for value, include earnings trends, cash flow, future growth rate, and a company’s book value.

“The problem with Cisco now is many of those measures, particularly earnings, aren’t stable,” says Ghriskey. “The more those earnings go down the more expensive Cisco’s stock becomes.”

Lippman, who runs the Franklin Value Fund, says that generally-speaking value fund managers like himself are loathe to touch a stock unless it’s trading closer to 8 to 12 times earnings, and only then if the company has other factors, such as a strong growth rate or compelling book value working in its favor. (Book value refers to the value of a firm’s hard assets).

“Most of the big name technology stocks don’t swing into our vision because of the remaining valuation issues,” he says.

In short, Lippman says picking value stocks involves far more than looking for once expensive names that can now be had on the cheap.

“Just because a stock has come down 75 percent it doesn’t mean it’s a value,” Lippman says. “It’s possible it could have been overvalued by 90 percent.”