Oracle: Another Moment of Truth

Oracle: Another Moment of Truth

By Hal Plotkin

CNBC.com Silicon Valley Correspondent

Mar 27, 2001 03:34 PM

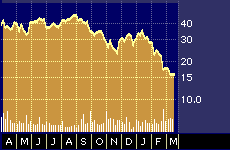

Oracle 52-week stock performance

The analyst, who leaped ahead of the pack in predicting Oracle’s recent steep stock decline, remains bearish on the software maker despite the company’s continued optimistic projections about its near-term future performance.

But unlike last summer when Robertson Stephens analyst Eric Upon made his controversial call, he’s no longer the only skeptic in the analyst community on whether Oracle Corp. {ORCL} will meet the sales and profit targets needed to prevent further declines in the stock.

At present, 22 security analysts tracking the stock are sticking with their “buy” or “strong buy” ratings. About 30 analysts track the Redwood City, Calif., company. Five others have downgraded the stock in recent months in a signal of increasing concerns about whether the company will meet its sales and earnings targets for the remainder of the year.

The biggest issue facing Oracle’s shareholders is the amount of projected business back-loaded into the end of Oracle’s current fiscal year. For his part, Upin says investors are likely to hear more bad news coming out of Oracle later this year even though most analysts have already reduced their forward-looking earnings and revenue expectations after Oracle’s recent earnings miss.

Working off his own recently shaved estimates, Upin says the immediate future looks more than challenging for Oracle.

“On the applications side Oracle must now close almost 40 percent of this year’s number in Q4,” says Upin. “On the database side they need to close almost one third of this year’s business in Q4. The growth rate needed to do that is almost 60 percent from the third quarter to the fourth quarter. That’s a huge, huge number, and a huge risk to the fourth quarter.”

On March 15, Oracle reported third-quarter earnings of $583 million, or 10 cents a share, compared with $503 million, or 8 cents a share, for the same period last year. Two weeks earlier the company had warned that its profits would be 2 cents per share less than the 12 cents most analysts had expected. Guidance going forward, which the company’s CFO labeled “a guess,” calls for flat earnings growth during the fourth quarter based on an expectation of flat database revenues and growth in sales of online applications in the range of 15 to 30 percent.

In addition to contending with the economic slowdown, Oracle is also weathering charges of improper insider trading.

In January, just a few weeks before the company announced the earnings miss that sent the stock into a tailspin, Oracle founder Larry Ellison sold 29.2 million Oracle shares earning a gross profit of almost $900 million. In March, Ellison said the earnings miss came as a complete surprise to top executives at his company, himself included, and was the result of an unexpected number of last-minute delays in closing deals toward the end of the quarter.

As is common in such cases, several shareholder lawsuits have since been filed alleging misconduct on the part of Ellison and other senior executives at the firm related to the insider stock sales. The company maintains the charges are without merit and will be contested vigorously in court.

If Ellison was surprised by the earnings miss, however, Upin was not. And he says investors should not be surprised if Oracle misses again when it reports fourth quarter earnings in mid-June.

“I did get a lot of nasty looks,” recalls Upin about his late summer warning that Oracle’s stock was heading for a fall. “But it seemed clear to me even then that they were going to have a lot of trouble making their numbers.”

Upin made his initial prediction when Oracle’s stock was flying high at over $40 a share. At the time Upin was a minority of one: 27 other analysts following the company had either “buy” or “strong buy” ratings on the stock.

Mark Jarvis, Oracle’s chief marketing officer, says he still thinks Oracle has the right products and strategy needed to meet its objectives. But he concedes that a worsening economy could put a damper on those hopes.

“The one thing we do not know about is the overall economy,” he says. “We’re being honest in saying we don’t know which way it is going to go. What we can control is our execution, which has been flawless lately.”

In particular, Jarvis says Oracle’s soup-to-nuts approach to e-commerce, which involves selling a suite of software, called 11i, to handle an entire company’s online information technology needs will prove superior over time to the strategy of its arch-rival, International Business Machines Corp. {IBM}, which is instead working with a number of leading “best-of-breed” more niche-oriented software providers in a series of well-publicized marketing relationships.

But not everyone agrees with Jarvis on that score. A recent report from Redwood City, California-based Zona Research, for example, called the current climate the “best of times for IBM and its partners,” and the “worst of times for Oracle.”

“To the recent woes over stock machinations and repeated bugs in its much touted B2B (business to business software) suite, Oracle must now cope with a world where more firms are standardizing on IBM,” concluded the authors of Zona’s March 19 report.

“The way we are going to beat IBM is with speed,” counters Oracle’s Jarvis. “We can get most customers up and running in 90 days,” he says.

Even so, Jarvis concedes it has taken longer than 90 days for the company to fully install its 11i software suite, which was formally introduced last May, inside Oracle itself.

“We now expect that process to be done in June of this year globally across Oracle,” he says. “Implementing our software in 90 days wasn’t so easy,” he says. “But that’s because it is also about changing and rebalancing business practices to be more efficient. We’re coming out of it in a much stronger position.”

As for the reports of bugs within the new software, Jarvis says they are a natural consequence of bringing any new software product to market. He also says the economic slowdown should help Oracle in its battle with IBM in the months ahead because cost-conscious corporate customers will increasingly prefer to purchase Oracle’s less expensive and more comprehensive packaged software solutions rather than pay consultants at firms such as IBM to integrate products made by a variety of vendors.

Jarvis might be relieved to know that no one, Upin included, is counting Oracle out of the fast-moving e-business infrastructure game.

“Oracle is a great company with a strong position,” says Upin. “Given the recent decline in valuation we do think it’s time for investors to start asking the question about when is the right time to pull the trigger and buy the stock.”

That time will come, says Upin. “But it’s not here just yet. We’ve only had one downward revision [to sales and revenue projections]. Often it takes two or three more until we get to the real base numbers [from which growth resumes].”

“All I can say is we are making good progress and selling as much as we can,” says Jarvis.