No Quick Cisco Fix

No Quick Cisco Fix

By Hal Plotkin

CNBC.com Silicon Valley Correspondent

May 10, 2001 04:34 PM

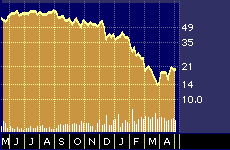

Cisco Systems 52-week stock performance

Like jilted suitors returning to a past love, investors have bid Cisco Systems Inc.’s {CSCO} stock up off the bottom it hit last month in hopes the company will ride out its current difficulties and start acting like its former self again sometime soon.

But this week’s earnings news and growing worries about Cisco’s future growth rate have dashed those hopes among many professional stock watchers.

“We’ll see a gradual recovery for Cisco over time,” says Martin Pyykkonen, an analyst at C.E. Unterberg, Towbin, based in San Francisco. “But it’s not going to be a sharp rebound. There’s no over-arching catalyst to spark things in a somewhat dormant environment.”

On Tuesday, Cisco Systems posted the first quarterly loss in its 17-year history, shedding $2.69 billion, or 37 cents a share, for its third quarter ended April 30. The figure includes a $1.17 billion charge connected to the firing of roughly 8500 full-time workers, and a $2.2 billion write-down of inventory the company says is outdated. Excluding those charges, Cisco earned 3 cents a share for the quarter on a pro-rata basis, one cent higher than First Call Corp.’s consensus analyst expectation.

Many seasoned observers aren’t paying much attention to the pro-rata earnings number because most of the excluded charges appear central to Cisco’s core business. The big story this week is the huge loss, not the balance sheet gymnastics that led to the illusion of a positive earnings surprise.

Some analysts have speculated that Cisco took the huge inventory write-off all at once as a way to get most of the bad news behind the firm and to set up the possibility for an upside earnings surprise in subsequent quarters. They reason that Cisco’s earnings could get a nice pop at some point in the future if the company finds a way to recycle some of the written-off inventory into products it can eventually sell. That view is supported by the fact that Cisco has not announced any plans to dispose of its excess inventory, for example, through industry liquidators, but is instead keeping the goods in storage.

Others see the inventory write-off an as ominous sign that Cisco is dangerously out of touch with its end-user markets.

Approximately 80 percent of Cisco’s inventory write-off was for raw materials such as memory chips, optical supplies, and nearly $1 billion in other chips and microprocessors. Supplies of that type can become obsolete very quickly because of rapid product lifecycles in the networking industry.

A report from Redwood City, based Zona Research, published on Wednesday after the earnings release, took Cisco to the woodshed for so badly miscalculating demand.

“However Cisco’s self-imposed melodrama plays out,” the report concludes, “the bottom line for information technology firms is that demand forecasting requires more than just assuming that the upward slope of past sales charts will continue forever. It also means being able to understand one’s products, markets, operations and people well enough to clearly look forward based on what is happening and what is likely to happen.”

The Zona report speculates that some of the inventory Cisco wrote-off will in fact find its way back into sales channels despite the fact that Cisco’s chief financial officer has said that won’t happen.

“We believe that they may be quietly engaging in channel stuffing, and that not all the $2.2 billion is a lost cause,” the report notes. “[But] this kind of bet-on-the-come sales forecasting is simply a hangover of past excess arrogance.”

The more important question now is whether those miscalculations will continue into the future, and, in particular, whether Cisco’s networking market business will grow at the long-term 30 to 50 percent annual rate currently forecast by the firm.

Given the company’s huge size and the law of large numbers few analysts are betting on that to happen. Cisco posted $23.9 billion in revenue last year, which means the company would have to add more than $4.7 billion in new sales next year to achieve even a twenty percent growth in revenues.

There are, however, some big questions about exactly how that can happen.

“While there were signs of improvement in some segments, the business outlook in the majority of Cisco’s markets remains challenging in the near term,” wrote Michael Ching, an analyst at Merrill Lynch, in a post-earnings report on that company.

Ching maintained his firm’s luke-warm “accumulate” rating on the stock, but raised his risk assessment to a C (above average risk) from a B (average risk).

Pyykkonen, at C.E. Unterberg, Towbin, says it’s possible that Cisco’s stock could move up to the $30 to $35 range over the next year, with $40 a share possible in “a year plus.”

But he says he wouldn’t be surprised to see the company’s growth rate fall well below current company projections.

Over the short term, Pyykkonen adds that Cisco shareholders could suffer further as a consequence of the cost-cutting in corporate America that is designed to protect balance sheet bottom lines.

“We’ve got a lot of layoffs in tech companies and non-tech companies and I don’t think the effect of that has really been felt yet,” he says. “The first thing that a good MIS (management information system manager) or CEO does when that happens is look for ways to reuse networking capacity that has become available, frankly, because there are less people around. I think we’re going to see more belt-tightening across the board.”

Although it has fallen dramatically off its highs, Cisco’s stock, which is still trading in excess of 30 times next year’s expected earnings, also seems unlikely to get much support from value fund managers who look for bargains among beaten-down securities.

“We almost never buy a stock trading at 30 times earnings,” says Bill Lippman, president of the $85 million Franklin Value Fund {FRVLX}.

Lippman says that, generally-speaking, value fund managers like himself are loathe to touch a stock unless it’s trading closer to 8 to 12 times earnings, and only then if the company has other factors, such as an indisputably strong growth rate or compelling book value working in its favor. (Book value refers to the value of a firm’s hard assets).

Some analysts think the current environment has placed something of a floor under Cisco’s stock, which has moved up slightly in recent weeks in sympathy with other Internet stocks that also appear to be flirting with their support levels. Cisco’s fortunes depend in part on the overall health of the Internet economy.

The basket of Internet stocks tracked by U.S. Bancorp Piper Jaffray, for example, gained more than 35 percent in April.

“We believe this gain represented the market’s attempt to establish a floor for the key Internet names,” says Safa Rashtchy, an analyst at U.S. Bancorp Piper Jaffray.

But Rashtchy warns that the run up in share prices appears to based on hope, not reality.

“The interesting point,” he says, “is that there are no changes in fundamentals that would warrant the increase in share prices.”