Intel’s Visibility Only Half the Battle

Intel’s Visibility Only Half the Battle

By Hal Plotkin

CNBC.com Silicon Valley Correspondent

Jun 8, 2001 03:38 PM

Investors gave Intel Corp. {INTC} credit this week for accurately predicting the degree to which its business is faltering. That good will won’t last long without improved results.

On Thursday, Intel held a mid-quarter conference call to announce that revenue and earnings for its second quarter, ending June 30, will come in within the earlier forecast range but somewhere below the mid-point of those previous predictions. In April, Intel has said it expected second-quarter revenue of $6.2 billion to $6.8 billion, expenses of $2.2 billion to $2.3 billion and gross margins of about 49 percent.

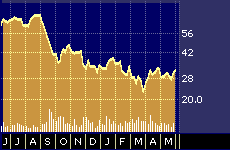

Intel Corp. 52-week stock performance

Intel’s revenue for the preceding quarter totaled $6.7 billion, which was down 16 percent from the first quarter of 2000 and down 23 percent from the prior quarter.

Intel’s stock rose roughly 15 percent in the days preceding the latest announcement as investors bought on the rumor of re-affirmed guidance. The stock fell back slightly Friday as at least some investors sold after the news was confirmed later in the week.

But several veteran chip-sector watchers warn that knowing you’ve stumbled is not the same thing as getting back up to speed.

“We encourage investors to take a long, hard look at the supply chain and end demand before buying Intel on a PC-recovery scenario,” says Merrill Lynch first vice president Joseph Osha, in a research note published this week.

CNBC.com: Envision the Tech Rebound

What worries Osha and others are indications of a potential stagnation in Intel’s key markets, most notably microprocessors. Those fears gained credence this week when Osha’s colleague, Jerry Labowitz, downgraded the stocks of component and connector makers Amphenol Corp. {APH} and Molex Inc. {MOLXA}, as well as electronic distributors Arrow Electronics Inc. {ARW} and Avnet Inc. {AVT}, all of which are considered vital links in the high-tech food chain.

Slackening demand for connectors, components and electronics distribution would seem to indicate continued weak demand for Intel’s products.

Chip stocks rose as a group this week, however, with many market watchers crediting an optimistic forecast from the Semiconductor Industry Association. On Wednesday, the chip makers’ trade group released its mid-year forecast, projecting an industry-wide recovery in the second half of this year and growth of 20.5% in 2002 and 25% in 2003.

But investors banking on those numbers had better hope they prove more accurate than the prediction the same group made last year, which called for revenue growth of 25 percent in 2001. The association’s most recent figures confirm that chip revenue will actually decline by 22 percent this year, which means the trade group’s 2000 projection overestimated 2001 demand by 47 percentage points.

“The inventory overhang was something we didn’t project,” says Molly Marr, spokesperson for the Semiconductor Industry Association. “The high amount of inventory from suppliers was something we couldn’t see that far in advance, not until the water was turned off in February.”

Marr says her organization used the same methodology to develop this year’s projection as was used last year.

“We have the same level of confidence,” she says. “It’s based on the companies’ best hopes of what they think is going to happen. Like last year, we are very confident about our [press] release.”

What’s not clear, however, is where all that growth is going to come from, particularly if economic conditions worsen. Many experts say that even if the economy does stabilize or recover, Intel must still deal with saturated markets and stiff competition from its archrival, Advanced Micro Devices Inc. {AMD}.

“How can you grow off a base of 135 million units shipped?” wondered George Gilbert, portfolio manager of the Northern Technology Fund {NTCHX}, during an appearance on CNBC-TV’s Business Center on Thursday.

Gilbert says the PC sector’s growth rate over the last five years is unsustainable. It is, he says, a matter a basic math.

Gilbert calculates that in order for the PC sector to grow at a modest (given its own track record) 10-percent annual rate from here, PC makers would have to sell more than 700 million new personal computers over the next five years.

“I know there is a replacement cycle, but who is going to buy all those new PCs?” he asks.

That could explain why U.S. Bancorp Piper Jaffray analyst Ashok Kumar titled his report on Intel’s announcement, “A False Dawn?”

In addition to worries over end markets, Kumar also says he has concerns that Intel’s investment portfolio could contribute to disappointing earnings. Last year, Intel generated almost $4 billion in capital gains, a performance that will not be repeated this year, when income from investments is expected to show no net gain.

“Without the boost from investment gains, the underlying base of earnings could be lower than expected,” warns Kumar, who nonetheless maintained his 12-month price target of $45 on the stock which is based largely, he says, on expectations of a seasonal rather than cyclical recovery in demand.

“Sentiment around the PC sector is so extreme that, due to seasonal effects, we should have a trading rally into the second half [of this year],” he says. “If you want to speculate, follow optimists first and switch to pessimists as reality emerges.”

Late Friday, Intel shares traded at $30.75.