PeopleSoft Gaining on Oracle

PeopleSoft Gaining on Oracle

By Hal Plotkin

CNBC.com Silicon Valley Correspondent

Jun 19, 2001 03:47 PM

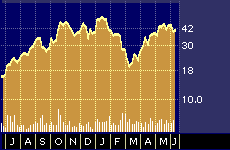

PeopleSoft 52-week stock performance

Oracle Corp. {ORCL} got all the attention this week, but several analysts think the comparatively stronger performance at rival Internet software maker PeopleSoft Inc. {PSFT} could be the bigger news in the months ahead.

Earlier this week, Dain Rauscher Wessels analysts Cameron Steele and Karen Haus initiated coverage of Peoplesoft’s stock with a “buy-aggressive” rating and a 12-month price target of $50 a share.

“This is a slight premium to other e-business application software vendors, but justified in our view due to PeopleSoft’s strong competitive position,” they wrote.

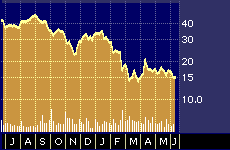

Oracle 52-week stock performance

PeopleSoft competes with Oracle, SAP AG {SAP}, Siebel Systems Inc. {SEBL}, and others in the enterprise resource planning (ERP}, supply chain management (SCM) and Customer Relationship Management (CRM) markets, all of which are increasingly Internet-based.

Unlike Oracle, which has it roots in the database market, PeopleSoft has been focused on human resource management applications from its inception in mid 1980s.

The analysts who prefer PeopleSoft say a comparison of recent financial results demonstrates that the company’s existing business footprint has put it in the superior position when it comes to cracking open the new business-based Internet application markets on which future growth depends.

In April, PeopleSoft announced what Merrill Lynch vice president Craig Wood called an “in-your-face” first quarter, with revenues from software licenses growing to $153 million as compared with the $143 million that analysts, on average, had forecast. PeopleSoft’s earnings per share for the quarter came in at 11 cents, as compared with the nine- cent consensus analyst forecast.

“It’s important to note that our [PeopleSoft] forecasts were not reduced on the heels of Oracle’s [then-recent] miss or other events, so these targets were relatively difficult to achieve,” Wood noted at the time.

Contrast that with Oracle’s announcement this week that it had beaten the analyst community’s consensus earnings estimate for its forth quarter, which was reduced in May, by a penny per share, but only by cutting costs, not by growing revenues. Oracle’s software licensing revenue actually declined 10 percent over the most recent quarter, to $1.656 billion, down from $1.84 billion in the same period last year.

Some observers feel that PeopleSoft’s success is coming directly out of the hides of Oracle and its other competitors.

“PeopleSoft’s product offering is the most comprehensive suite of Internet applications available,” write Steele and Haus, of Dain Rauscher Wessels, who note that PeopleSoft spent $500 million and more than two years of development time to build the company’s flagship applications suite, called PeopleSoft 8, which is largely responsible for getting sales back on track.

Some experts say that it will take some more time, and more customer experiences, to fully determine which Internet application suites work best, and for which types of customers. But industry analysts are generally, although not universally, impressed with PeopleSoft’s progress.

“We take a slightly positive stance on PeopleSoft,” concludes a report published on Tuesday by Current Analysis, a market and industry research firm based in Sterling, Virginia.

“There is strong uptake for the company’s PeopleSoft 8 architecture and associated e-business application,” according to the Current Analysis report, which was authored by analysts Kelly Spang and Jill Jenkins. “Nearly a year after PeopleSoft first debuted its Internet-based architecture, the company’s gamble with its PeopleSoft 8 architecture is clearly paying off.”

PeopleSoft’s relative strength is also reflected by overall analyst sentiments, with the current number of strong buy ratings on the stock now at 4, up from 2 two months ago. The number of strong buy ratings on Oracle’s stock, in contrast, declined from 5 to 4 just prior to this week’s earnings announcement, according to Zacks Investment Research.

Likewise, while Oracle is now projecting flat revenues next quarter, PeopleSoft still sees more growth ahead. PeopleSoft’s most recent guidance for the full year, which was updated in late April, calls for 35 percent license growth in 2001 and earnings per share of between 55 to 60 cents.

“It seems fair to conclude that more than ample business remains in the backlog and pipeline to achieve targets for the second quarter and the remainder of the year,” writes Wood, of Merrill Lynch.

Industry analysts at Zona Research, however, warn that it would be a mistake to make too much of the fact that PeopleSoft is getting traction in the Internet applications market at a time when Oracle appears to be mostly spinning its wheels, particularly in the slowly-developing online customer relationship arena.

Things could change quickly, according to the Zona analysts, if and when a CRM vendor provides end-user customers with more noticeable service improvements.

“Few of these offerings are designed to really improve the customer experience,” according to Zona’s more critical recent report. “Instead they offer convenience and efficiency to the company deploying the CRM package. We have to wonder at what point will customers start turning away from companies that view them as nothing more than a resource to be strip-mined.”

The Zona report goes on to note that, in the future, competitive CRM suppliers will have to take the word “relationship” far more seriously and improve the experiences of the end-users of such software programs if they are to deliver the increased revenues many market-watchers anticipate.