Analysts Predict i2 Comeback

Analysts Predict i2 Comeback

By Hal Plotkin

CNBC.com Silicon Valley Correspondent

Jul 9, 2001 11:32 AM

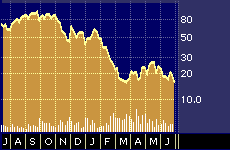

i2 Technologies Inc. 52-week stock performance

Shares of i2 Technologies Inc. {ITWO} fell 20 percent last week after the company pre-announced a larger-than-expected loss for its fiscal 2001 second quarter ended June 30. But several company watchers from both financial and industry analysis firms have stepped up their efforts to defend the firm, saying i2’s success with major customers confirms that it is selling what may well be the single most comprehensive and best-integrated business-to-business software suite now available.

On July 2, Dallas-based i2 said it anticipates reporting a pro forma second quarter net loss of about 12 cents a share, excluding a $25 million to $27 million (4 cents a share) bad-debt charge from losses related to sales charge-offs, most notably from failed dot-com customers. Analysts were expecting i2 to post a loss of 6 cents a share for the quarter, according to First Call Corp.’s consensus estimate.

On the positive side, analysts note that i2 still has more than 1000 customers, including many big names such as The Boeing Company {BA}, Ford Motor Company {F}, Dell Computer Corp. {DELL}, and United Parcel Service {UPS}.

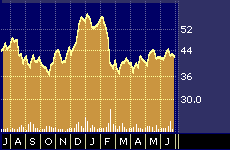

Nike Inc. 52-week stock performance

Earlier this year, however, i2 got a notable public relations black eye, which also hurt the firm’s stock, when one of its big customers, Nike Inc. {NKE}, claimed that problems associated with the installation of i2’s software had played a major role in its own highly-publicized earnings miss.

But analysts following the B2B market say that despite the damage done to the stock by Nike’s claims and the current economic slowdown, i2 is still posting strong repeat business from what otherwise appears to be a loyal and still-growing customer base.

“Nike issues are now a non-issue,” states Merrill Lynch analyst Chris Shilakes in a research note published shortly before i2’s recent warning.

Shilakes says his checks with customers indicate that the Nike controversy is no longer affecting i2’s sales channels, if it ever did. Instead, he says sales have been dampened along with those of similar firms over the past few months primarily as a consequence of the slowing economy.

“[i2’s] repeat customer business remains high, which signals strong customer satisfaction,” he says.

Shilakes reiterated his lukewarm accumulate/high risk rating on the stock late last month in anticipation of the recent earnings warning. But like several other analysts, he’s decidedly more upbeat about i2 over the long-term.

“I2 remains the gorilla in supply chain management, which we believe remains a significant, multi-year opportunity,” he says. “The company is a long-term core holding, despite the near-term difficulties the present environment presents.”

Jefferies & Company analyst Richard Williams is even more positive and says investors should buy the stock when others shun it.

Williams says he thinks the worst might be over for i2 and that the company is also doing a good job of cutting expenses. Williams has a $28 12-month price target on the stock, based on 10.5 times the firm’s forward revenue, which he says in line with other major competitors whom he did not name.

“We would buy i2’s shares on weakness,” Williams says, in a research note published just after this week’s earnings warning.

Although worries persist about how i2’s stock might fare should the economy continue to slide, industry analysts who don’t participate in the securities business also confirm that i2 has a very solid product portfolio.

“i2 continues to offer the most robust and technologically advanced e-business solution in the marketplace,” according to a current company assessment produced for private clients of market research firm Current Analysis, based in Sterling, Virginia.

“Each of the distinct components of i2’s offering have outdistanced its respective competitors,” says the Current Analysis’ profile of the firm. “Together these products form a very cohesive offering that customers can quickly take to market.”

Last year, i2 became the first e-business solutions provider to top $1 billion in annual revenue. But the success came at a very steep price, with the firm posting an eye-catching net loss of $1.75 billion, or $4.83 for each common share.

“I’m disappointed with our recent results, and am committed to making the necessary adjustments to continue our leadership and the achievement of our vision,” pledged i2 CEO Greg Brady in a statement that accompanied this week’s earnings warning.