Sanmina Can’t Buy Demand

CNBC.com Silicon Valley Correspondent

Jul 19, 2001 11:13 AM

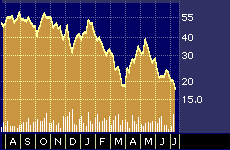

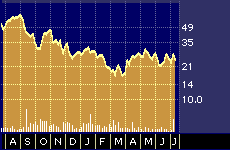

SCI Systems 52-week stock performance

SCI Systems 52-week stock performance

Sanmina Corp.’s {SANM} purchase of larger rival SCI Systems Inc. {SCI} will create a formidable player in the electronics manufacturing services sector (EMS), but bloated inventories and weak demand will likely keep a lid on all EMS stocks, analysts warn.

A rebound may not materialize until later this year or well into next, industry watchers say. Sanmina on Monday offered to acquire SCI Systems for $6 billion in stock and debt.

“SCI and Sanmina should gain leverage to help win more contracts in the longer term,” says Lehman Brothers’ analyst Louis Miscioscia, in a research note published after this week’s deal was announced. “However, in the near term we don’t expect a change in the competitive landscape.”

Like Miscioscia, most analysts who follow the leading EMS players still see plenty of growth ahead for the outsourced manufacturing sector. That may help explain why the basket of EMS stocks tracked by Merrill Lynch was up roughly 65 percent, as a group, between their lows in March and early April and the peak they hit in early June.

“Investors should keep in mind that we have witnessed periods when industry conditions improved over a couple of quarters but gave a false signal of a sustained recovery,” says Merrill Lynch analyst Jerry Labowitz in a research note published on Wednesday.

Labowitz cites 1997 as an example, a year when he says it appeared the electronics supply chain sector had hit bottom, only to tank further during the first three quarters of the following year.

Sanmina, which has long focused heavily on the supposedly high-margin telecommunications and optical assembly markets, announced that it would purchase SCI Systems, which has diversified operations somewhat in recent years but has it roots in servicing the traditionally lower-margin assembly needs of the personal computer industry.

Both firms, however, have encountered significant difficulties in recent quarters as demand for Sanmina’s higher-margin telecommunications products nose-dived while SCI’s personal computer markets flat-lined.

In general, analysts are taking a positive stance on the acquisition, seeing it as a way for both firms to hedge their bets by further diversifying their customer base while increasing the ability of the combined firm to serve global customers through a greater number of facilities.

There are also expected to be opportunities for cost-cutting as a result of the consolidation, with Robertson Stephens’ analyst Keith Dunne predicting the merged firm might cut about 10 percent of headcount shortly, assuming there is no uptick in end user demand.

“We view this transaction favorably, as it broadens Sanmina’s portfolio, expands its capabilities and geographic presence,” writes Labowitz in a research note.

But overall, he notes, the EMS industry is now dealing with some major changes.

In recent years, for example, up to 60 percent or more of EMS revenue growth has come directly from increases in outsourcing, with the rest coming from organic growth in end-user tech markets.

But the recent steep, some say almost unprecedented, decline in many end-user markets, most notably telecommunications, is taking place at the same time when analysts are suggesting that annual growth in outsourced manufacturing will probably now tail off to no more than about 15 to 20 percent because so many large firms have already made that move.

“Further signs of deteriorating demand for communications equipment with little hope on the horizon does not bode well for most of the EMS providers we follow,” says Labowitz.

The big issue, he says, are the excess inventory levels. At the end of the first quarter of this year, for example, Labowitz calculates that EMS firms, on average, had 68 days of inventory on hand, as compared with the average of 43 days.

In the overall electronics supply chain, he says, that means there is around $16 billion dollars of inventory that must now be worked down before the tech industry gets back to a more normal order flow.

“Our overall view on this deal is lukewarm,” says Miscioscia, of Lehman Brothers. “It could take a while to gain the possible benefits of the merger and near term prospects remain clouded.”

Likewise, Labowitz says the overall EMS sector has now entered uncharted territory.

“Our long-term enthusiasm for the secular trend to outsourcing remains intact,” he wrote in a research note he released last month explaining why he was maintaining long-term buy ratings on the leading EMS firms.

But in today’s more recent update reviewing inventory issues in the overall electronics supply chain, Labowitz sounded a decidedly more dire note.

“The velocity of this downturn,” he added, “has surpassed any other period of decline over at least the last 10 years.”

The Merrill Lynch analyst now says that given current trends it will take until at least around the middle of next year to work down tech inventories to more traditional levels.