Straight Story on Align Tech

Straight Story on Align Tech

By Hal Plotkin

Silicon Valley Correspondent

Feb 27, 2001 03:58 PM

Now that Align Technology Inc.’s {ALGN} post-IPO quiet period has ended, the securities firms who took the company public are out with a series of lengthy initiation reports that suggest the stock is headed for 50 percent or more price appreciation over the next 12 months.

While that kind of cheer leading is to be expected from the company’s financial backers, leaders in the field of orthodontics agree that upstart Align is successfully carving out a role for its new teeth-straightening technology in a large and growing market.

There are some questions, however, about exactly how big a place it will be. The bigger question, though, is whether the company can live up to expectations and its own projections fast enough to attract the institutional investors that would create and sustain the healthy returns promised for early buyers of the stock.

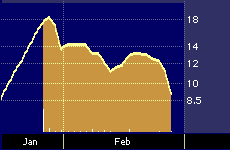

Align Technology post-IPO stock performance

Align went public on January 26 with shares initially priced at $13 each. The stock shot up about 30 percent on its first day of trading but has since slid back to a few dollars under its offering price.

“Align does appear to have a niche for its corrective appliance in some small percentage of adults,” says Dr. Michael Rennert, president of the American Association of Orthodontists. “So far it appears to be useful in treating only minor problems, but there is definitely a role for new braces in treating adults, whether it is braces with colors or just plain clear braces, or wires that go behind teeth or [Align’s] Invisalign product.”

Align’s financial backers, not surprisingly, are painting a much rosier picture.

“In our opinion, the potential market opportunity for Align Technology’s Invisalign System is massive,” says Rick Wise, an analyst at Bear Stearns, based in New York. Wise’s firm took Align public along with J. P. Morgan, Robertson Stephens, and Deutsche Bank Alex. Brown.

Wise says there are about 200 million people in the U.S. alone suffering with some form of crooked teeth, more formally known as malocclusion.

“The number of potential patients dwarfs such common conditions as vision impairment (140 million people) and hypertension (55 million),” he says. “Yet, with only 2 million people seeking treatment each year, or 1% of the total prevalence, malocclusion remains an extremely underserved market.”

Align’s system is ideal for some significant portion of untreated adult patients, Wise says, because it addresses the most common obstacle to getting treatment: unsightly and often uncomfortable braces.

The company’s novel technology works by creating a series of clear, customized, removable dental appliances that move teeth to their desired position over a period of time. Unlike conventional braces that need to be monitored and tightened by trained professionals, Align’s system delivers results while requiring less time and effort on the part of orthodontists.

The product, which is useful in less severe cases, typically costs patients slightly more than conventional approaches, $5500 versus $4000 per patient, on average. But orthodontists who use the system can generate income of roughly $1,300 per hour, as compared with the roughly $450 per hour they receive over the course of standard orthodontic treatments, because of fewer patient visits.

That may explain why nearly two-thirds of the 8,500 U.S. and Canadian orthodontists had already accepted training by the company in the use of the new technology as of the end of last year. That number is expected to grow to 75 percent by the end of March, according to the company. Overall, 9,300 patients were treated in 2000, with a projected increase to over 37,000 cases this year, and more than 178,000 in 2003.

On Monday, the company reported a net loss of $66.3 million for the year ended December 31 on revenues of $6.7 million, as compared with a net loss of $15 million on revenues of $400,000 for the prior year. According to the company, the losses are largely attributable to the expansion of manufacturing capacity, the funding of a national consumer advertising campaign and the continued development of product and manufacturing process technology.

At year-end Align had cash on hand and short and long-term marketable securities of $18.7 million, total assets of $70.6 million and a stockholders’ deficit of $84.7 million, a figure that includes outstanding accounts payable, accrued liabilities and deferred stock-based compensation.

The company’s hopes now rest on whether enough of the estimated 99 percent of untreated adults with crooked teeth hear about and seek out the new treatment over the course of the next year or two.

Dr. Rennert, the orthodontics association president, says it could happen, particularly if the economy recovers to the point where more adult consumers feel free to spend money taking better care of their teeth.

“There are health benefits that come from straighter teeth,” he adds, noting that attention to such concerns can prevent more significant problems later on. Rennert says that’s one reason adults currently constitute approximately 20 percent of the average orthodontic practice patient load.

“That could go up if people feel they have more discretionary income so they can afford some more perks for themselves,” he says.

This week’s less than stellar earnings announcement was followed by a roughly 10 percent sell-off in the stock. Nonetheless, the four analysts who initiated coverage last week are sticking with their buy ratings and 12-month price targets, which range from $17 to $30 a share. They say they big ramp up is just ahead for the company, in terms of revenues and profits.

But Gary Craven, portfolio manager for Evergreen’s Small Cap Growth Fund, says it will probably be a while before Align’s stock attracts the attention of large institutional buyers of securities.

Craven says the big money players will probably hold back for a while given Align’s dwindling financial resources to make sure the company is ramping up the number of new patients served as promised. One way to get an early indication that is happening, he says, is to look for trends in the stock’s daily trading volume, which must go up from current levels to give institutional buyers better assurances they will have the liquidity they prefer.

“It’s exactly the kind of stock we look at,” he says. “But we need to see a little more.”

Craven says individual investors would be smart not to wager too heavily on the company at the present moment.

“The best strategy for a stock like this is to make small bets,” he says. “It might do very well if they can execute. But you want to make a number of small bets on firms like this because there’s a number of them that won’t work out.”