What’s Next for Yahoo!?

What’s Next for Yahoo!?

By Hal Plotkin

CNBC.com Silicon Valley Correspondent

Apr 5, 2001 08:00 AM

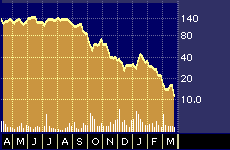

Yahoo! 52-week stock performance

In an unusual twist, several leading industry analysts paint a rosy long-term picture for Yahoo! Inc. {YHOO} at the precise moment when many usually more positive securities analysts are recommending a hands-off approach to the company’s battered stock.

Disagreements between securities analysts, whose firms sell financial services to tech firms, and industry analysts, who advise companies on major technology purchases, are not rare. But the disagreements usually went the other way during the market’s long run up, with securities analysts typically pushing stocks while industry analysts often poured cold water on the assumptions behind those recommendations.

Given the recent market drubbing, however, that situation is starting to turn around, at least in some instances.

In Yahoo!’s case, for example, many securities analysts who got burned by the stock’s precipitous fall over the past year have backed away from it. The number of “strong buy” and “buy” ratings on Yahoo!’s stock has dropped to 12 from 18 three months ago. More telling, five analysts have slapped “sell” ratings on Yahoo!, a rare development in an industry where securities firms are typically reluctant to antagonize potential corporate customers by issuing negative recommendations about their stocks.

Many of these now-negative financial analysts say they need to see more visibility into Yahoo!’s earnings before they can once again put the stock back on their recommended list.

But several leading industry analysts say their colleagues on Wall Street have overreacted to the recent Yahoo! earnings shortfall that sent the stock tumbling. To be sure, none of them are recommending buying the stock, since they don’t offer advice about securities purchases. But they do say the future is not as bleak as the stock’s recent performance would seem to indicate.

“Yahoo!’s dismal short-term prospects don’t detract from the basic strength of the company,” writes Eric Scheirer, an analyst at Forrester Research, based in Cambridge, Mass., in a recently published research report on the company.

Scheirer says Yahoo!’s “deep understanding” of the Internet and prominent position as a leading Web portal will see the firm through the tough times, notwithstanding recent difficulties. Among Yahoo!’s urgent needs is a new CEO to replace the resigning Tim Koogle, who will stay on as chairman.

The theory among the industry analysts goes something like this: With more than a billion Web pages served per day, Yahoo! commands the traffic that will make it the locus of whatever happens next online, including the creation of new advertising techniques that take better advantage of the online medium’s still-growing popularity.

“I hate to back up one of our competitors,” says Andy Bartels, an analyst at the Giga Information Group, which also advises corporate customers on strategic issues. “But I have to say I agree with the Forrester conclusion. Yahoo! and AOL are clearly the two top leaders in that space. That leaves them very well positioned as the place where the biggest, traditional advertisers are going to look to experiment and try new approaches to online advertising.”

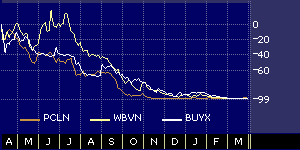

Priceline.com, Webvan and Buy.com 52-week stock performance comparison

Bartel’s optimism is noteworthy, in part, because he’s long been one of the leading skeptics regarding online business plans, having accurately predicted the many problems encountered by first-generation business-to-consumer firms like Priceline.com Inc. {PCLN}, Webvan Group Inc. {WBVN}, and Buy.com Inc. {BUYX}.

The falloff in online advertising, particularly from dying dot-coms, was the prime factor behind the most recent slide in Yahoo!’s stock. Last month, Yahoo! announced that revenue for the first quarter, ended March 31, would come in somewhere between $170 million and $180 million, well below the $220 million or more most analysts were expecting. The company also said it expects break-even earnings when it reports quarterly results on April 11, down from the four cents most analysts had expected, according to First Call Corp.

The uncertainty over Yahoo!’s near-term future led to a slew of downgrades that pushed the stock down to a 52-week low of just over 11 a share.

“From a balance-sheet standpoint, Yahoo!’s drivers are pretty poor,” explains Matt Moberg, an analyst with Franklin’s $57 million Large Cap Growth Fund {FKGAX} who is among those avoiding the stock.

“Yahoo!’s business model is in transition,” he says, pointing to the company’s need to bolster ad revenue and diversify its income stream. “I would absolutely not be a buyer at these levels until we see a new business model that is working.”

“I think the stock goes sideways for the next couple of quarters,” adds John Corcoran, an analyst at CIBC World Markets Corp., based in New York, who has a hold rating on the stock.

“Yahoo will have a couple of bullet holes in it when all this is over,” he says, “but it’s not going to be another Pets.com. They have enough money in the bank so they can do deals. The franchise will survive.”

The big question overhanging Yahoo!’s future, say the analysts, is how long it will take to perfect new online advertising and marketing strategies that deliver more obvious returns on investment to advertisers.

“I can’t tell you how long that will take,” says Bartels, of the Giga Information Group. “But I do think we’re going to see the big advertisers doing it first, and the Yahoo!s of the world are the best place for those advertisers to experiment with new approaches. Once they can prove something works with the audience that Yahoo! Commands, it will trickle down to the smaller sites.”

Bartels notes, for example, that it took some time after television was invented before advertisers mastered the nuances of that medium.

“The cycle time on the Internet is going to be much faster because of the instant feedback,” he says. “That’s why I think we’ll see more volume from the traditional advertisers that should be sufficient to get Yahoo! back on its growth path.”

Moberg adds that Yahoo! remains a name that many investors would like to own, despite the significant losses Yahoo! investors have suffered over the past year.

“I do agree that people will come back to it once all this gets sorted out,” he says. “But we need to see more evidence that’s starting to happen.”