Ariba Answers Critics

Ariba Answers Critics

By Hal Plotkin

CNBC.com Silicon Valley Correspondent

Apr 25, 2001 05:00 PM

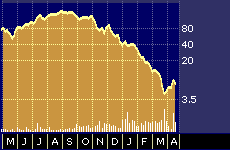

Ariba 52-week stock performance

Most experts say don’t look for much from Ariba Inc.’s {ARBA} stock over the next few quarters, with some warning that the company’s existing product line up might not be enough to assure the firm’s long-term survival, let alone its success. The tanked stock has been all but abandoned by analysts over the past month after the company’s big earnings miss and the scuttling of its high-profile merger deal with Agile Software Inc. {AGIL}.

The stock would be a great buy, however, if the company can get earnings growth back on track. In an exclusive interview earlier this week, company officials told CNBC.com that is exactly what will happen. But many of the analysts following the firm say it still looks like quite a long shot.

“Ariba’s average deal size peaked last year at $2 million and I think it’s going to go down rapidly from here,” says Tom Harwick, research director for supply chain management at Giga, based in Cambridge, Massachusetts. “They pioneered their part of the market but it’s not very complex so there are lots of new entrants. They still need to find a credible partner [to restore earnings growth].”

“We probably haven’t done as good a job as we should briefing the analysts about what’s happening,” counters Michael Schmitt, Ariba’s senior vice president and chief marketing officer.

A case in point, Schmitt says, are the average deal size figures which he says show the reverse, at least in so far as average sales of the company’s highest, end electronic procurement software products, which he says grew to $1.8 million per deal last quarter, up from $1.7 million during the previous quarter.

“Last year, the buzz about our company was probably more positive than it should have been. But the situation is reversed and there is now more negative buzz than there needs to be,” Schmitt says.

Schmitt freely acknowledges that last quarter’s big earnings miss was a major setback. But he says the analysts and investors who have bailed out of the stock over the past few months have overlooked the factors that will put it back on track: revenue growth and continued return on investment for customers.

“We’re going to survive this,” he says. “We’ve got over $300 million in the bank. But the real key is the tremendous customer stories about how Ariba has helped our customers save money. It’s our customers who will keep us going through the bad times.”

Schmitt says he disagrees with most analysts tracking the firm who say that Ariba doesn’t have the right product mix needed to restore earnings momentum.

“I don’t think they understand our company,” he says.

It’s hard to find a firm that has taken a bigger bashing from analysts in recent weeks. The analysts were mortified when Ariba’s earnings for its second quarter came in so far below consensus analyst expectations as to make Ariba this earnings season’s worst performer relative to expectations among the nine major B2B platform providers tracked by U.S. Bancorp Piper Jaffray. Ariba missed its numbers by almost twice as much as the average of its key competitors during the last quarter.

Last Friday, Ariba posted revenues of $90.7 million for its second quarter ended March 31, 2001. The firm’s pro-forma net loss for the quarter came in at 20 cents a share, far worse than the six cents in positive earnings analysts had expected before Ariba warned of a pending shortfall earlier in the month.

“The Street was shocked by the magnitude of the 2Q 01 earnings miss,” Christopher Shilakes, an analyst at Merrill Lynch, wrote in a research note published after the firm pre-announced the disappointing numbers. “We cannot remember when a company with a revenue base of this scale missed street estimates by more than 50 percent.”

Shilakes downgraded the stock to “neutral,” saying Ariba’s performance left little room for hope over the near-term. He isn’t alone. Fourteen other financial analysts have downgraded Ariba’s tanking stock over the past three months from previous “strong buy” ratings to less enthusiastic “buy” or “hold” ratings. All told, 28 analysts now rate the stock a “hold,” which indicates that they do not believe it is an attractive place for investors to put fresh money.

According to critics, the underlying problems confronting Ariba, beyond the poor recent financial performance, center around the firm’s focus on what is called the materials, repairs, and operating supplies (MRO) market. The MRO B2B market, which Ariba pioneered, consists mostly of the basic, low-margin supplies and equipment needed in typical office settings, as compared with the higher-end direct materials procurement business, which revolves around supplying manufacturers with raw materials and components used to make products. Ariba generates about 90 percent of its revenue from the MRO market, according to the Giga Information Group.

“Ariba is facing a very big problem in that they are stuck in the MRO ghetto,” says Harwick, of the Giga Information Group. “They will get no traction at all if they keep doing what they are doing.”

Schmitt, of Ariba, disputes that, and claims that analysts are missing a key point.

According to his calculations, manufacturers spend approximately 33 to 35 percent of their money on MRO supplies.

“That’s where we started because that is where we could deliver the fastest return on investment to customers,” he says. “We’re now branching into the direct materials.”

Essentially, Schmitt says, the company has used the lower-margin MRO market as a way to build a diverse base of customers, which include American Express Co. {AXP}, Dell Computer Corp. {DELL}, and Southwest Airlines Co. {LUV}. The earnings miss, he says, was primarily related to an unexpected slowdown in Ariba’s software sales stemming from the economic downturn.

“We have 8500 suppliers, 10 million lines of [product] catalog entries, and over 100,000 purchase orders being written per month right now,” he says, referring to Ariba’s Commerce Services Network. “Our pitch is that if you are in business and you buy stuff, and you want to save money, you should call Ariba, because we do that best.”

Schmitt adds that none of the B2B competitors who have targeted the higher margin direct materials supply business, which include Commerce One Inc. {CMRC}, I2 Technologies Inc. {ITWO}, and Oracle Corp. {ORCL}, can match Ariba when it comes to its linked network of MRO suppliers and customers. Schmitt says that puts Ariba in a niche, which he calls the value chain, that is certain to expand. (What Schmitt calls the “value chain” others often call the “supply chain”).

“What I think people are missing is that when you are talking about the value chain there are a multitude of [software] applications that still need to be written,” he says. “No one owns that market yet because it is still wide open. So we feel we have a head start.”

Schmitt says that Ariba’s failed merger with Agile, which spooked many investors, was the result of the adverse market conditions that depressed his firm’s share price.

“Agile had one process we wanted to add but because of the economy we couldn’t go through with the deal,” he says. “But it was only one process out of many. Ariba has a $425 million run rate and Agile has a $71 million dollar run rate. So they lost more [cross-selling] than we did.”

Schmitt would not predict when the overall economy will recover or when that recovery will begin to show up on Ariba’s balance sheet. But he says the company expects to deepen its relationships with its existing customers and will continue to attract new customers as it diversifies and improves its product offerings.

“We still grew our revenues by 126 percent last quarter year over year,” he says. “We’re rebuilding and getting back to basics by emphasizing return on investment for our blue chip customers.”

Ariba got a little good news on Friday when Salomon Smith Barney analyst Gretchen Teagarden bucked the tide and upgraded the stock to “market perform,” saying she thinks the worst is now behind the firm.

But the majority of other analysts tracking the stock say they need to see more proof that Ariba will be able to defend its margins going forward.

“In the MRO area they face the danger of having the same problem the spell-checker vendors had,” says Karen Peterson, research director at Gartner, based in Stamford, Connecticut. “Spell-checkers were sold as a standalone application but all those companies went out of business when spell-checking was bundled with other products. I would be very cautious about Ariba because MRO won’t be enough unless they have more progress to show in supply sourcing.”

“We’re just going to keep helping our customers save money,” counters Schmitt, who says further product development efforts and an economic recovery will eventually restore investor confidence in Ariba.