Valuing VeriSign

Valuing VeriSign

By Hal Plotkin

CNBC.com Silicon Valley Correspondent

Mar 13, 2001 10:45 AM

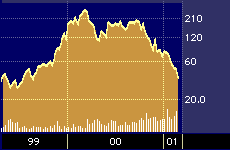

VeriSign 2-year stock performance

It seemed a bit like old times on March 1 when Dain Rauscher Wessels analyst Stephen Sigmond reiterated his firm’s “strong buy-aggressive” rating on VeriSign Inc.’s {VRSN} stock, along with a sky-high $185 12-month price target.

Although $185 would not get the stock anywhere near its 52-week high of $259 a share, the move Sigmond forecasts would represent more than 300 percent appreciation from the point at which he made his call.

Instead, however, the exact opposite has occurred, at least so far, with the stock shedding yet another 20 percent of its value over the last two weeks.

The latest setback for VeriSign investors doesn’t, however, surprise many other analysts tracking the company and the stock. Many of those analysts say that VeriSign’s biggest challenges still lie ahead, despite the good news that touched off Sigmond’s renewed enthusiasm.

Sigmond did not return CNBC.com’s call requesting an interview. He did outline the reasons for his optimism about the stock in his research note, which centered on the agreement VeriSign recently reached with ICANN, the Internet Corporation for Assigned Names and Numbers.

Last year, VeriSign acquired Network Solutions, Inc., the original monopoly registrar of all Internet domain names.

The acquisition was somewhat controversial at the time, given the many fervent calls within the online industry for the addition of competing Internet domain name registrars and domain name suffixes (such as .person and .store). Several analysts have warned that the addition of new domain names and new registrars could significantly lessen the value of VeriSign’s acquisition of Network Solutions.

Questions have also been raised about whether VeriSign’s domain name registry will be of much practical help to the company as it seeks to attract customers to the other, higher-margin portions of its stable of product offerings, which include network security and a variety of other business-related online services, such as online payment processing and web site design.

Then, late last month, ICANN, which serves as the Internet’s de-facto governing body, reached a new deal with VeriSign that will upon final approval extend the company’s role as the monopoly registrar of all Internet web sites ending with .com through November 2007, after which time it will have what the contract language calls the “presumptive right” to renew.

In addition, VeriSign will also remain the exclusive registrar of all Internet web sites ending in .net until January 1, 2006, after which time that franchise will be put up for bid.

VeriSign receives $6 for per domain name per year. The company’s current registry contains approximately 25 million registered .com and .net domain names.

“By keeping its [dot com and dot net] registrar, VeriSign will preserve a large source of revenues and operating cash flow, as well as a strategic vehicle for cross-selling and up-selling complimentary services to its customers,” Sigmond wrote in his optimistic assessment.

Not so fast, say a slew of other analysts.

“The deal with ICANN is good news for VeriSign,” agrees Andrew Bartels, an analyst at the Giga Information Group, based in New York. “But I’m hard-pressed to see how it will have the kind of impact that’s being talked about.”

Bartels has been right in the past. He predicted the rapid decline in the stock prices of many once-leading dot com retailers, such as Priceline.com Inc. {PCLN} and Buy.com Inc. {BUYX}, back when those firms first went public.

He’s not predicting a further steep decline in VeriSign’s stock at the present time. But he says investors will likely get burned if they buy-in to the notion that developments related to the recent ICANN-related deal will push the stock back up anywhere close to its previous highs.

The Giga analyst also notes that ICANN finally appears to be on the verge of authorizing several new Internet domain name suffixes that VeriSign will not control. And he also has doubts about whether the company’s role as a registrar will translate into substantial new business opportunities for its other product lines, all of which are focused in areas where competition is rather stiff.

Preston Dodd, an analyst at Jupiter Media Metrix, based in New York, says Verisign’s registry, and in particular, the dot com portion, is valuable in that it is one of the few parts of the Internet infrastructure that can’t easily be replaced by some competing approach.

“Dot com is the Internet’s gold mine,” Dodd says. “It’s what people think of when they think of the Internet.”

Dodd is quick to add that he also doesn’t see how the recently inked deal can triple the company’s present value.

“I can’t say anything about the stock price,” he says. “But the registry process itself is not going to triple anyone’s business.”

Dodd does hold out some hope, however, that VeriSign will be able to further develop and enhance its complimentary lines of business as a result of the new arrangement with ICANN, in particular, by helping companies handle global domain name registrations to protect trademarks internationally.

“The real value is VeriSign’s access to the database, which gives them the name of somebody at each company who is authorized to sign a check,” Dodd adds.

But as Dodd and others see it, sales leads are not the same as sales. Which means VeriSign still must prove the synergies between its registry business and other operational areas.

And it’s precisely that uncertainty that has discouraged more interest in the stock among many potential institutional buyers, says Martin Whitman, chief investment officer at the Third Avenue Value Fund.

“In general, I think there are a lot of tremendous bargains among the cratered Internet stocks,” says Whitman. “But the problem is they are almost impossible to analyze. That’s why so many other analysts have failed so miserably when it comes to predicting the dot com future. They’re trying to do something that really can’t be done at this point.”

Representatives of VeriSign were not immediately available for comment.