IBM Still Has Safety Net

IBM Still Has Safety Net

By Hal Plotkin

CNBC.com Silicon Valley Correspondent

Apr 18, 2001 08:00 AM

Investors and corporate customers seeking security in uncertain times are expected to continue to protect International Business Machines Corp.’s {IBM} stock from the steep declines felt elsewhere in the tech sector.

IBM reports earnings for its first quarter after the market close on Wednesday.

The company is expected to earn $1.76 billion, or 98 cents a share for its first quarter, according to First Call Corp.’s consensus estimate. Sales are expected to come in around $20.7 billion, up about 7 percent from $19.3 billion one year earlier.

The stock fell off slightly on Monday but later recovered after J.P. Morgan analyst Daniel Kunstler shaved his first quarter revenue and earnings targets in a move that brought his numbers closer to the consensus estimate.

“The changes should be viewed as holding IBM’s earnings feet a bit further from the fire,” Kunstler wrote, adding that he still believes the stock, which he rates a “buy,” to be undervalued.

He’s not alone. The 21 other securities analysts following IBM have an average $138 12-month price target on the stock. Kunslter’s 12-month price target comes in on the high-end, at $150.

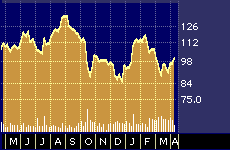

IBM 52-week stock performance

Of course, there are risks. Even analysts optimistic about IBM say they worry this earnings report will come with warnings of leaner times to come due to slowing economic growth here and abroad. But the difficult times are also expected to work to IBM’s advantage by driving increased numbers of skittish customers into Big Blue’s arms while consolidations in the industry reduce competitive pressures.

One main reason for the optimism among analysts and some fund managers is IBM’s well-cultivated reputation as a safe bet for both investors and technology buyers.

“In this climate some customers become concerned about viability issues,” says Shawn Willet, principal analyst at Current Analysis, a high tech consulting firm based in Sterling, Virginia. “A certain amount of customers will go with IBM just to be conservative. It’s a name the CEOs know and are comfortable with.”

“We expect to see IBM be an outperformer on a relative basis during weak economic times,” says Timothy Ghriskey, portfolio manager of the $2.1 billion Dreyfus Fund {DREVX}. Ghriskey’s fund is an IBM shareholder.

Ghriskey says IBM’s diverse product portfolio and recurring revenue streams gives the company more insulation than most against a slowdown in any one particular market. The company has been showing strength recently in its mainframe, server, database, and services businesses, which helps make up for weakness in the personal computer sector.

“You really shouldn’t put IBM in the same category with Hewlett Packard, Compaq, or even Sun,” says Gary Helmig, an analyst with Wit SoundView, based in Stamford, Connecticut.

Helmig notes that out of IBM’s total annual revenues of about $88 billion dollars in fiscal 2000 only about $12 billion came from personal computer related markets. The lion’s share of IBM’s revenues came from the sale of services, which pulled in roughly $33 billion last year, with non-PC hardware bringing in about $25 billion, followed by software sales, which accounted for about $13 billion in sales.

Like Kunstler, Helmig recently took down his estimates for the current quarter to account for the impact of the slowing economy. But even so, he says IBM’s complimentary product lineup contributed to a quarter that “looks very attractive operationally.”

The analysts say IBM should continue to provide a relatively safe haven for tech investors at least until the current economic clouds begin to clear. They add that the company is also likely to emerge from the current slump in better shape than most of its remaining competitors, although once the economy recovers tech investors will probably have to look elsewhere for more significant share price appreciation.

“Slowdowns tend to create consolidations that benefit larger companies,” says Willet, of Current Analysis. “But IBM’s strength is also its weakness. It will be stronger after the third tier players drop out or are consolidated. But once the economy recovers that whole cycle will start again and people will be paying more attention to companies with a more aggressive approach.”

Willet cites IBM-competitor BEA Systems Inc. {BEAS} as an example of a company that might outperform IBM in the end user markets in which it competes once the slowdown ends.

“There’s a huge fight going on between those two,” he says. “IBM benefits from the slowdown, but BEA has a huge number of partnerships and is executing extremely well.”

Ghriskey, the Dreyfus fund manager, says he might be looking to get out of the stock if he were to begin sensing an imminent economic recovery. He agrees that a recovery would probably work more to the advantage of IBM’s so-called “best-of-breed” competitors which, in the application server space, include BEA Systems.

But in the meantime he says the stock’s forward P/E multiple of 19 puts it in his fund’s sweet spot.

“It’s below the market averages at 19, which is very reasonable for a tech stock, and for IBM in particular.”

Willet notes that IBM has at least one other thing going for it.

“The company is definitely going to survive,” he says. “They can afford to have a few divisions that lose money for a while. That makes them a very tough competitor for companies that are only in one market.”